As of July 2025

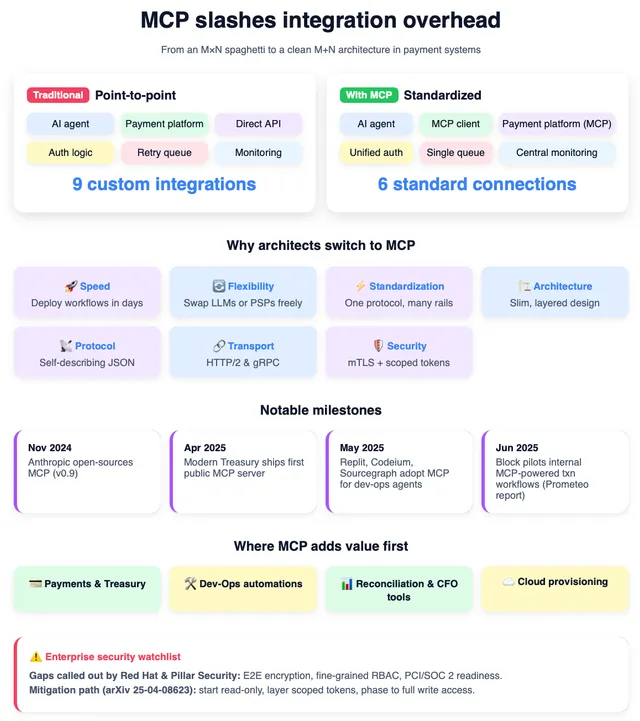

The Model Context Protocol is doing to payment integration what USB-C did to cables: collapsing a mess of custom connectors into one standard. The technology is ready enough to matter and not yet ready enough to trust with production money.

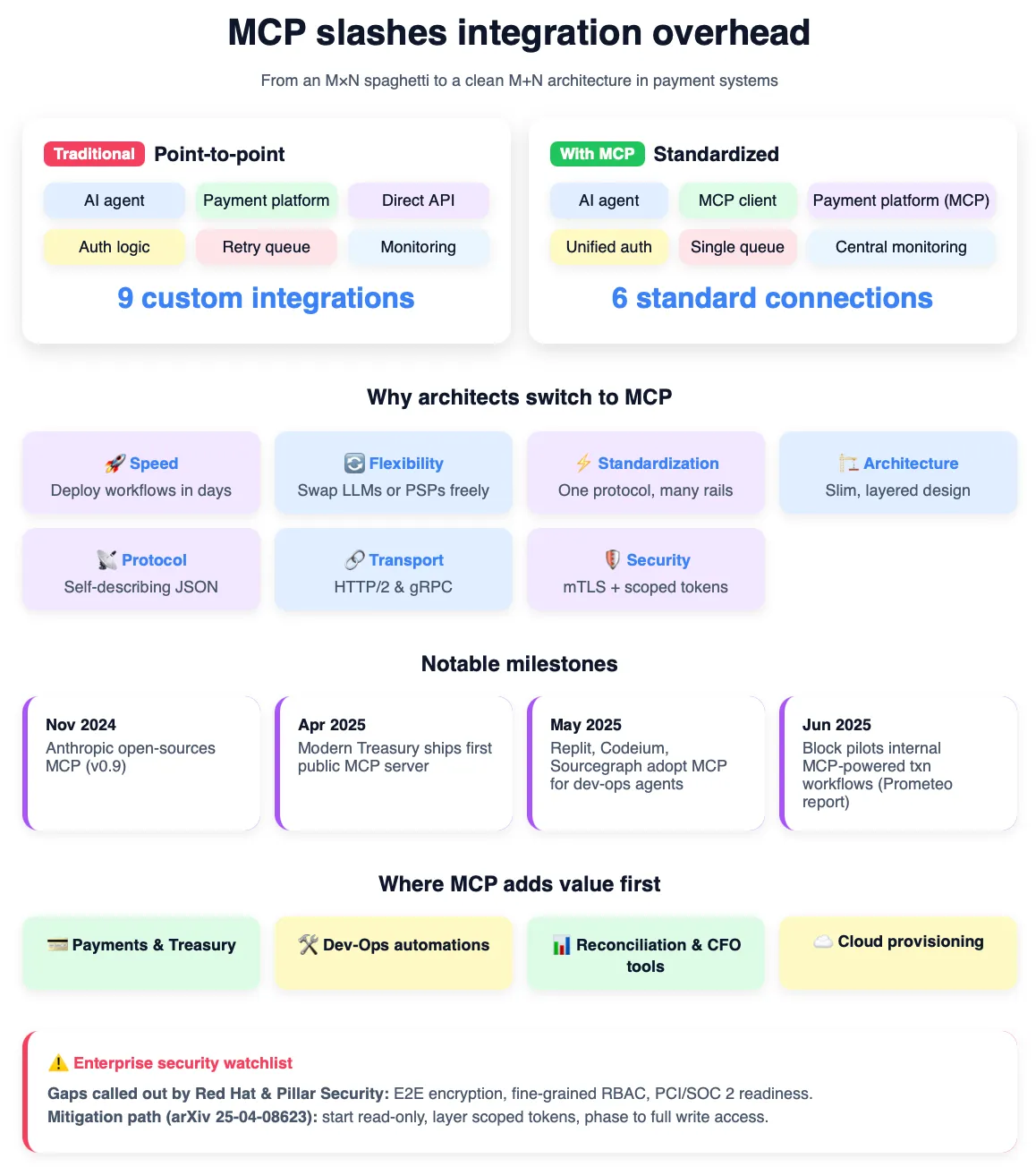

Most payment integrations still look like 2015 - custom code for every platform, months-long implementations, and rigid architectures that crack when requirements change. MCP changes the shape of that problem.

The old way: want your AI to create an ACH payment? Build a custom API wrapper. Need wires? Different code. Real-time payments? Start over. MCP replaces that with one standardized interface - build one MCP server per platform and one client per AI system, and the integrations stop multiplying. Anthropic open-sourced it in November 2024 as “a USB-C port for AI applications,” and by April 2025 Modern Treasury had shipped a payments MCP server with a demo of an agent creating an expected payment from a plain-English instruction. The shape is right.

Integration math

M + N

one MCP client per AI system, one MCP server per platform - instead of building MxN custom connectors that break on change.

Released

Nov 2024

Anthropic open-sourced MCP, "a USB-C port for AI applications"; Modern Treasury shipped a payments MCP server in April 2025.

Not enterprise-ready

Gaps

token theft, prompt injection, and a "keys to the kingdom" risk; missing fine-grained access and SOC 2 / PCI posture (Pillar Security, 2025).

The constraint is trust, not capability. Security researchers (Pillar Security, March 2025) flagged the obvious failure modes early: OAuth token theft, indirect prompt injection, and the “keys to the kingdom” problem where compromising one MCP server opens broad access to financial systems. Through mid-2025, MCP still lacked the enterprise controls banks require - fine-grained access, strong auditability, and a clear SOC 2 / PCI compliance posture.

This feels like the early days of REST APIs: promising technology with implementation gaps that the early adopters will be the ones to solve.