As of May 2026

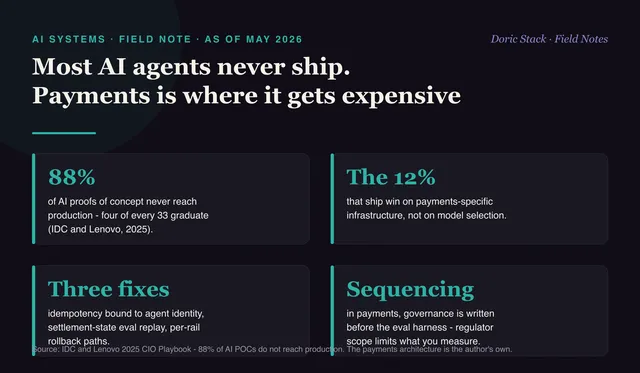

The headline number on AI agents is a failure rate. The widely cited figure is that 88 percent of AI proofs of concept never reach production. Agentic payments do not get a discount on that gap. They pay more for it.

The teams crossing into production are not winning at model selection. They are winning at payments-specific infrastructure that makes an agent observable, governable, and rollback-safe at the rail boundary. The ones still calling this a machine-learning problem will be in pilot when 2027 starts.

The gap is real, the cause is not the model

IDC and Lenovo’s 2025 CIO Playbook put the number plainly: about 88 percent of AI proofs of concept never make it to production, with only four of every thirty-three graduating. That figure is about AI projects in general, and agentic payments inherit it rather than escape it, because a payment agent has to be right about money, not just about language. The traits that separate the teams who ship are familiar enough to list - infrastructure, governance, baseline metrics, and clear ownership. What gets missed is the sequencing. In payments, governance gets written before the eval harness, because regulator-facing scope constrains what you are even allowed to measure. Visa has gone as far as predicting that in 2026 AI agents will complete purchases rather than just assist with them. That is the demand side. The supply side is whether your rails can survive an agent that retries.

What a payment agent breaks that a chatbot does not

A language agent that gets a fact wrong writes a bad sentence. A payment agent that gets the settlement window wrong moves money twice. The blast radius is different, so the controls have to be different.

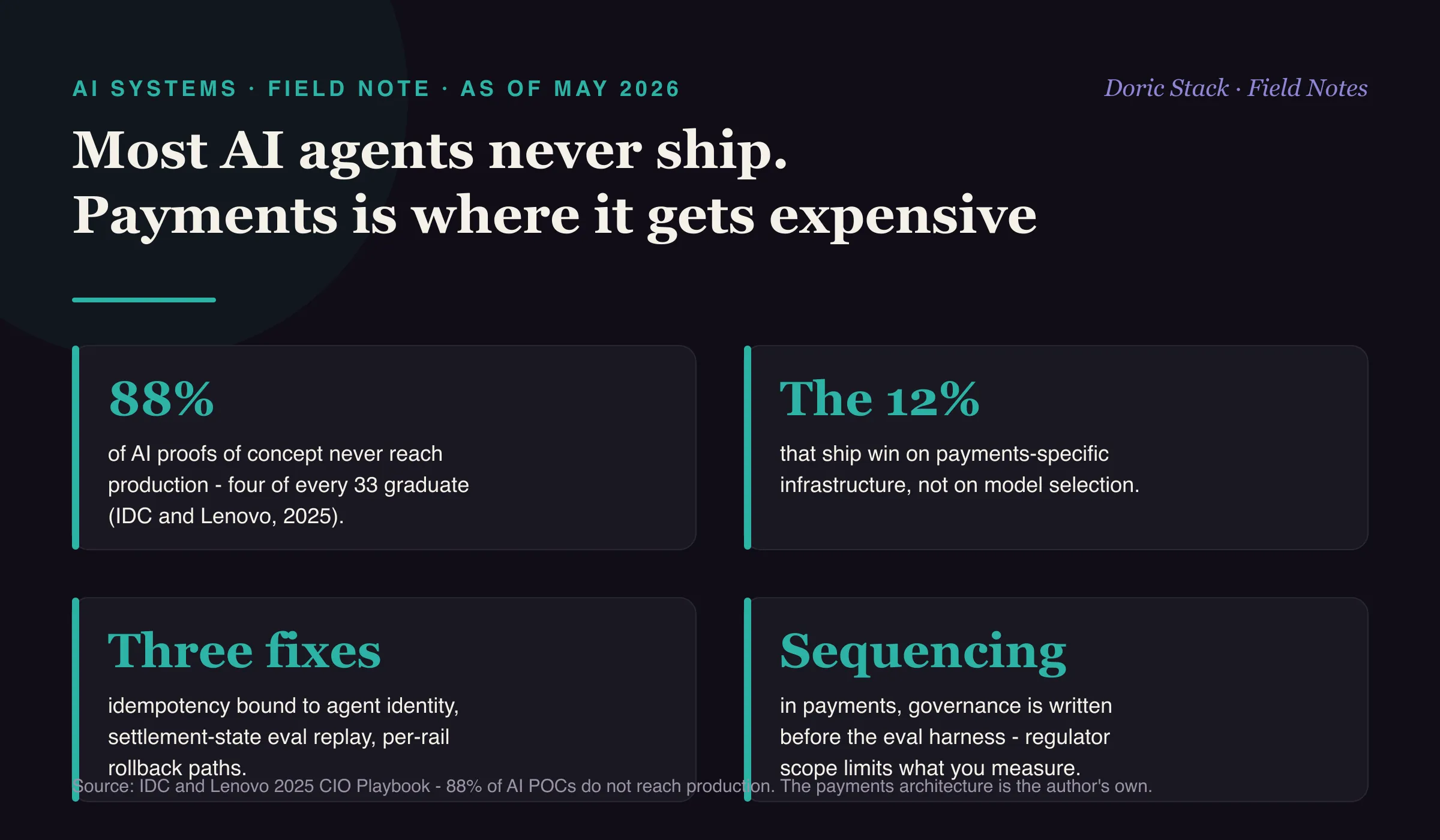

The production gap

88%

of AI proofs of concept never reach production - four of every 33 graduate (IDC and Lenovo, 2025).

Where the 12% win

Rails work

the agents that ship win on payments-specific infrastructure, not on model selection.

The three fixes

Rollback-safe

idempotency bound to agent identity, settlement-state eval replay, and per-rail rollback paths.

The three fixes that show up in production

The agent payment integrations that reach production share three controls, and none of them are about the model.

The first is idempotency bound to agent identity at the rail level. An agent retrying an ACH origination after a timeout cannot be allowed to create a second debit, so the NACHA originator record has to resolve back to the agent that initiated it. The second is an eval harness that replays settlement state, not just message correctness. A payment agent that gets the message right and the settlement window wrong is still a production incident, and a harness that only checks the message will pass it. The third is a rollback path defined per rail. RTP does not reverse the way ACH does, a FedNow Request for Return of Funds is not a wire investigation, and the escalation tree has to know which rail it is standing on before it does anything.

The 12 percent are not winning at model selection. They are winning at payments-specific infrastructure that makes an agent observable, governable, and rollback-safe at the rail boundary.