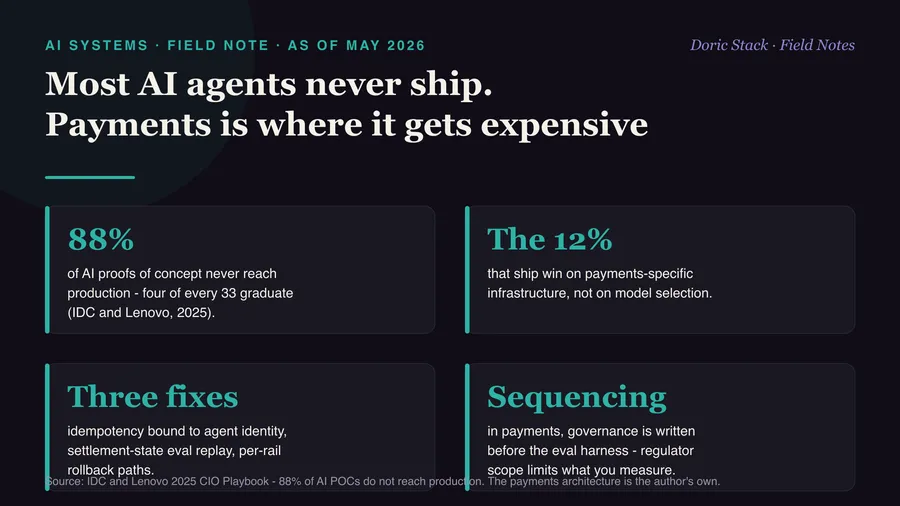

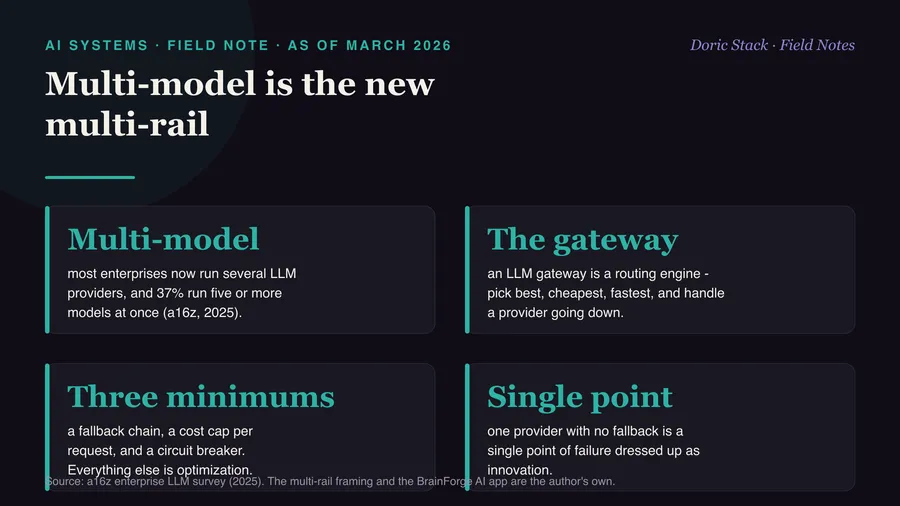

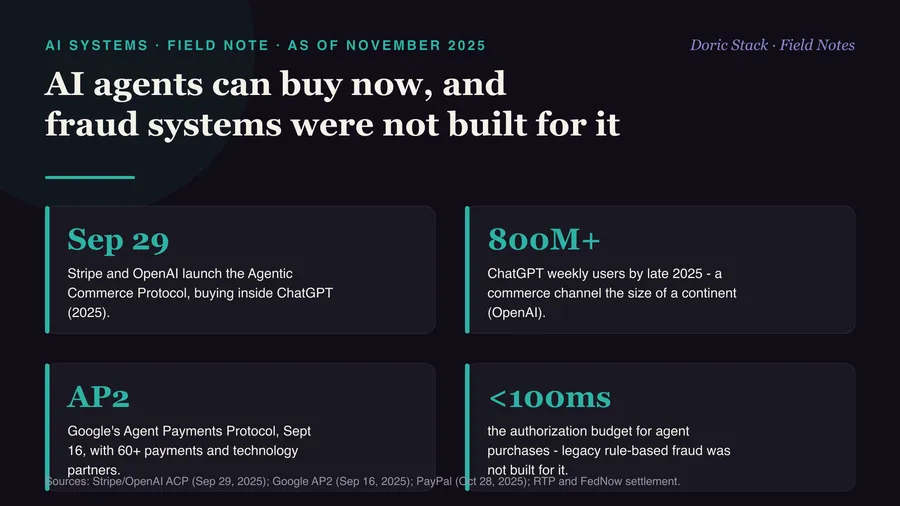

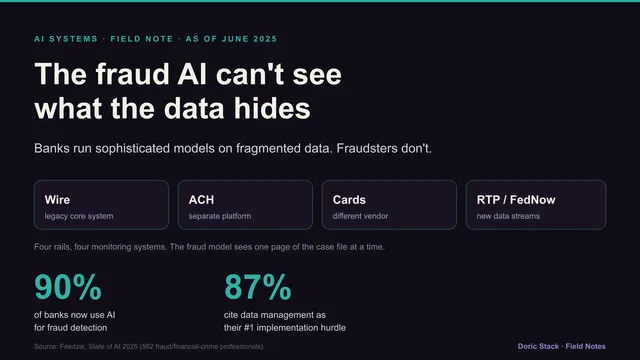

As of June 2025

The fraud AI is not the problem. The fragmented data underneath it is - and a model that sees one rail at a time loses to a fraudster who works across all of them.

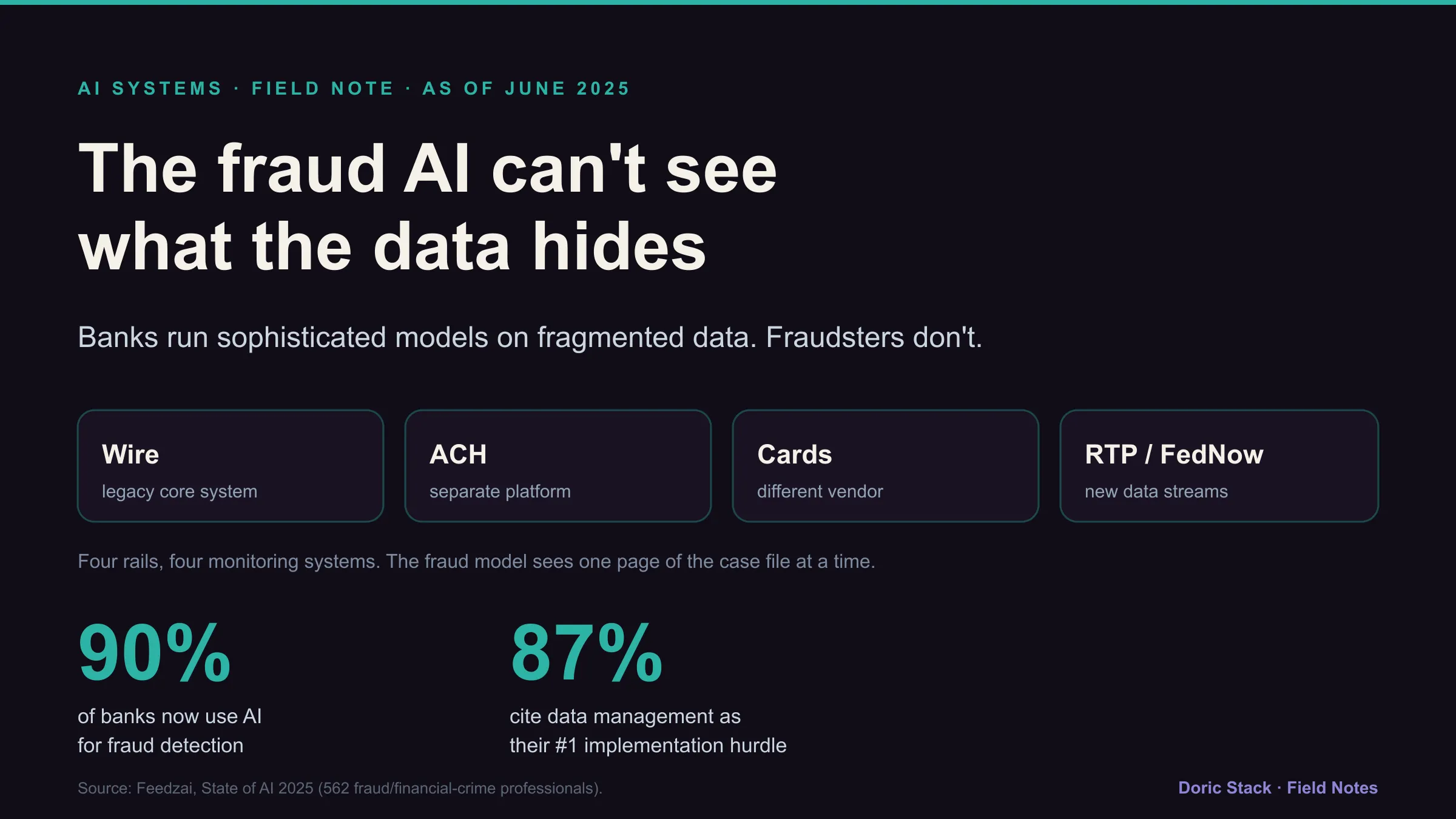

The fraud-prevention demos look amazing until you remember where the data actually lives: wire in one system, ACH in another, cards in a third. How is a model supposed to spot a pattern it cannot even see?

What the fraud model sees

One rail at a time. Wire transfers sit in the legacy core. ACH runs through a separate monitoring platform. Card activity belongs to a different vendor with different rules. The instant rails, TCH-RTP and FedNow, arrive as brand-new data streams bolted on last. Each system has its own view, its own rulebook, and its own idea of “normal.”

How the fraudster operates

Across all of them, on purpose. They test your wire limits, probe ACH for weak controls, then execute through instant payments where the money is gone in seconds. Their cross-channel coordination is better than most banks’ fraud systems, because the bank’s systems were never wired to compare notes.

Fraud AI's blind spot (June 2025)

The four monitoring silos a fraud model has to reason across, and the adoption-versus-data-readiness gap behind the problem.

Fraud AI's blind spot (June 2025)

The disconnect is structural, not cosmetic. Banks are deploying sophisticated machine-learning models on top of data architectures that were never designed to share a customer. Fragmented data leads to fragmented protection, and in fraud prevention partial visibility is almost as dangerous as none - it produces confident alerts on incomplete pictures.

Fraudsters don't operate in silos. Asking a model to catch them while showing it one rail at a time is like asking a detective to solve a case from random pages of the file.

AI adoption

90%

of banks now use AI for fraud detection - the model is no longer the hard part (Feedzai, State of AI 2025).

The real bottleneck

87%

cite data management as their biggest AI implementation challenge, not the algorithm.

The blind spot

4 silos

wire, ACH, cards, and instant rails monitored separately, so no single model sees the whole customer.

The banks making real progress are not just buying a better model. They are rebuilding the data layer first - a unified platform where the fraud model can see wire, ACH, card, and instant-rail behavior as one customer, not four strangers. The sequence matters: unify the data, then point the AI at it. Do it the other way around and you have bought an expensive detector for patterns it structurally cannot see.