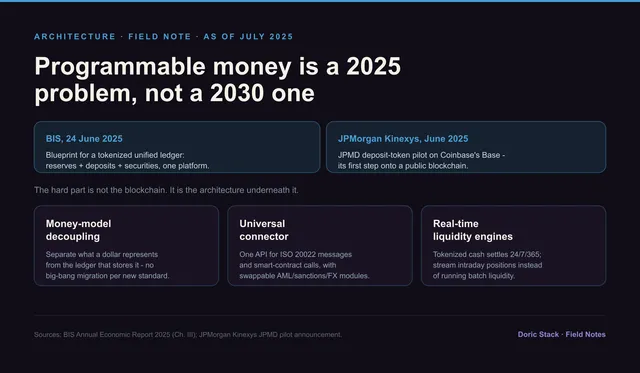

As of July 2025

Most banks are still planning tokenized-deposit strategy like it is 2019. The reference points moved this year - and the gap is architectural, not conceptual.

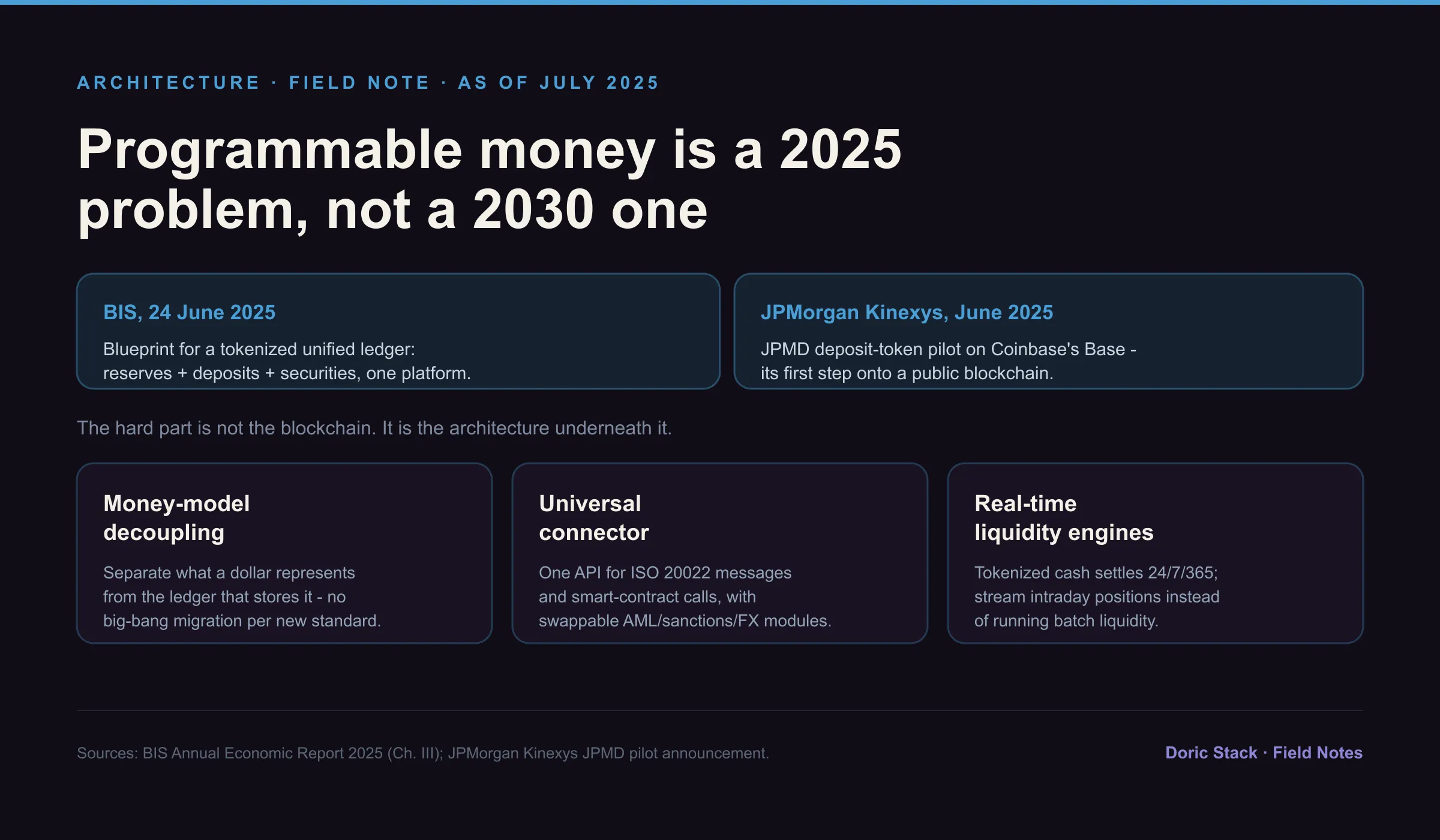

Two events landed within days of each other, and together they turned tokenized money from a 2030 slide into a 2025 design constraint for payment architects.

The BIS put it on paper

On 24 June 2025 the Bank for International Settlements released, in its Annual Economic Report 2025, a blueprint for a “tokenized unified ledger” - central bank reserves, tokenized commercial-bank deposits, and securities settling side-by-side on one programmable platform. It is the central-bank establishment describing programmable money as the next-generation system, not a fringe experiment.

JPMorgan put it in production

Days earlier, JPMorgan’s Kinexys unit began piloting a USD deposit token, JPMD, on Coinbase’s Base - an Ethereum public layer-2. After years running only on its private chain, it was the bank’s first step onto a public blockchain. A proof-of-concept, but a real one, on a public network.

The 2025 trigger and the foundations

The two June-2025 events that made tokenized money current, and the three architecture patterns that let a bank absorb it without a big-bang migration.

The 2025 trigger and the foundations

From modernizing payment platforms, the pattern is consistent: the blockchain technology is rarely the bottleneck. The bottleneck is retrofitting core banking architectures to support programmable money without breaking what already runs. Three design choices keep showing up as the ones that decide whether a bank is ready.

Money-model decoupling

No big bang

Separate what a dollar represents from the ledger that stores it, so a new standard plugs in without another core migration.

Universal connector

One API

Handle ISO 20022 messages and smart-contract calls through the same payment layer, with swappable AML, sanctions, and FX modules.

Real-time liquidity

24/7/365

Tokenized cash settles around the clock; stream intraday positions instead of managing liquidity in batch.

The complexity is not in understanding blockchain. It is in retrofitting core banking to carry programmable money without breaking existing operations.