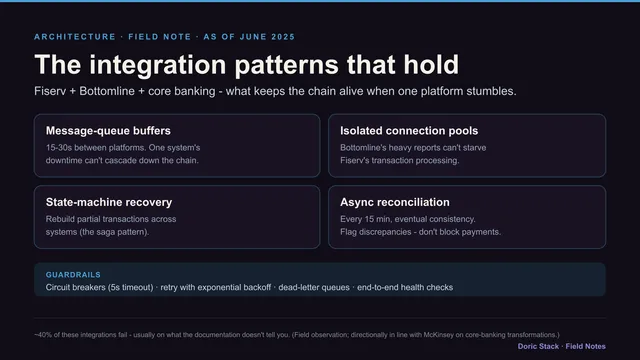

As of June 2025

The platforms work fine individually. Orchestrating Fiserv, Bottomline, and a core banking system into one payment chain is the hard part - and it comes down to a few unglamorous resilience patterns, not heroics.

In my experience these integrations succeed maybe 60% of the time. The other 40% become expensive lessons in what the vendor documentation does not tell you. The dividing line is rarely the feature list - it is how the seams behave when one platform stumbles.

The failure rate is not a vendor knock. Broader industry research on banking-technology transformations points the same direction: most large core-banking change programs fall short of their goals. The integrations that survive are not the ones with the best individual platforms; they are the ones that assume each platform will fail at the worst possible moment and design the seams accordingly.

Patterns that hold (June 2025)

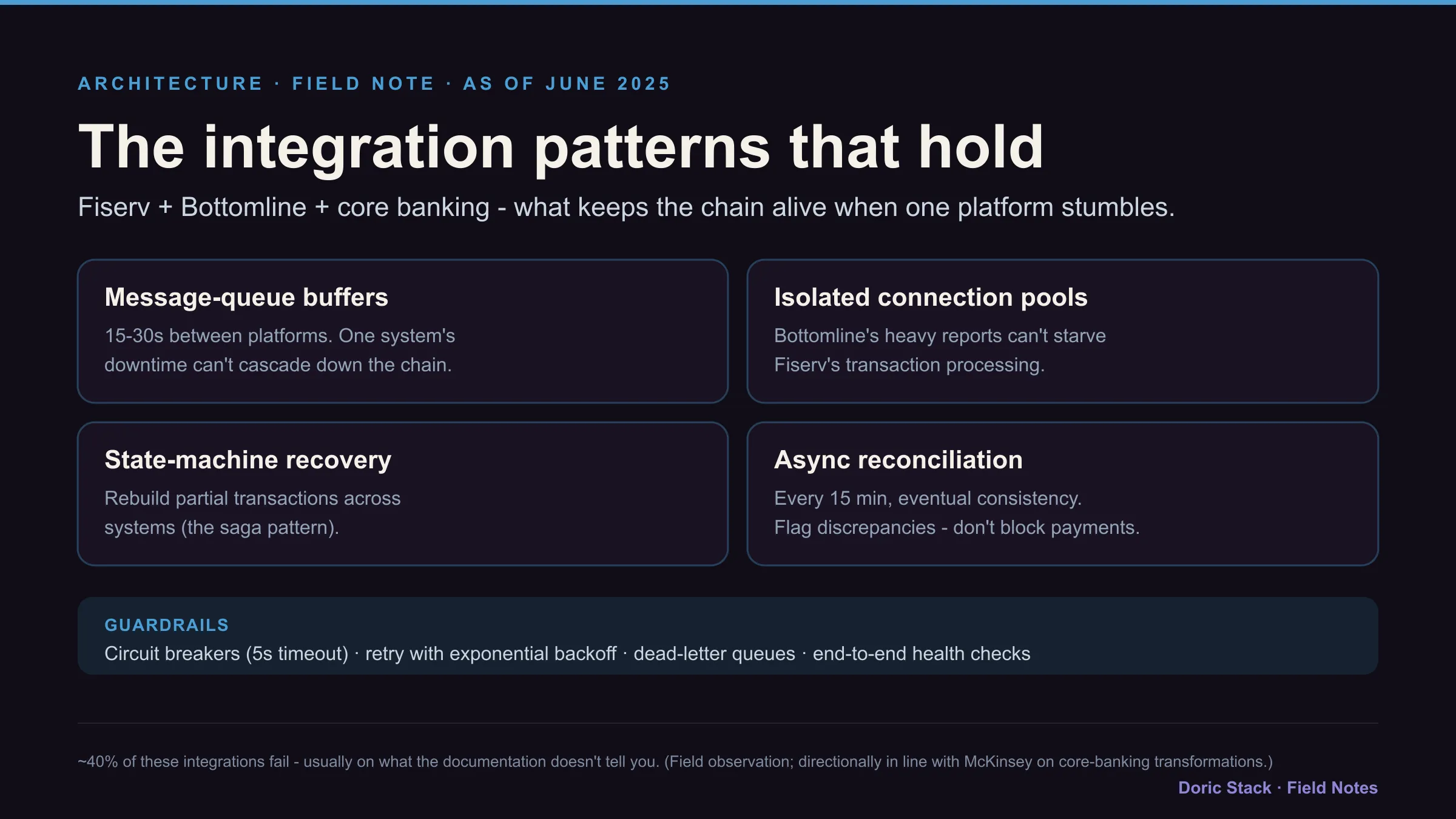

The four structural patterns plus the guardrails that keep a multi-platform payment chain alive when any one system degrades.

Patterns that hold (June 2025)

Keep the platforms from killing each other

Direct API calls between payment platforms create cascading failures, so put a message queue with a 15-30 second buffer between Fiserv processing and Bottomline workflows - one platform’s outage becomes a delay, not a chain failure. And never share connection pools: isolate the database connections per system, or Bottomline’s heavy reporting queries will starve Fiserv’s transaction processing. Separate pools, separate monitoring, separate alerting.

Assume partial failure, then recover

Payment platforms fail at different points in the transaction lifecycle, so build state machines that recover partial transactions across systems - when Fiserv has acknowledged a wire but Bottomline has not updated the balance, your recovery logic needs to handle exactly that. And stop pretending three systems reconcile in real time: run async reconciliation every 15 minutes, flag discrepancies for review, and never block a payment waiting on perfect consistency.

The guardrails around those patterns are what turn a good design into one that survives a bad night: circuit breakers with short (5-second) timeouts so a slow platform is treated as a failed one, retry with exponential backoff rather than constant hammering, dead-letter queues for transactions that fail repeatedly, and health checks that test the real end-to-end workflow instead of just pinging an API.

The platforms work well individually. The challenge is orchestrating them when each has different failure modes, recovery patterns, and operational characteristics.