As of June 2025

The instant-payments headlines celebrate volume. The average transaction sizes reveal what is actually happening: institutional money found a faster rail, and the consumer revolution is still years out.

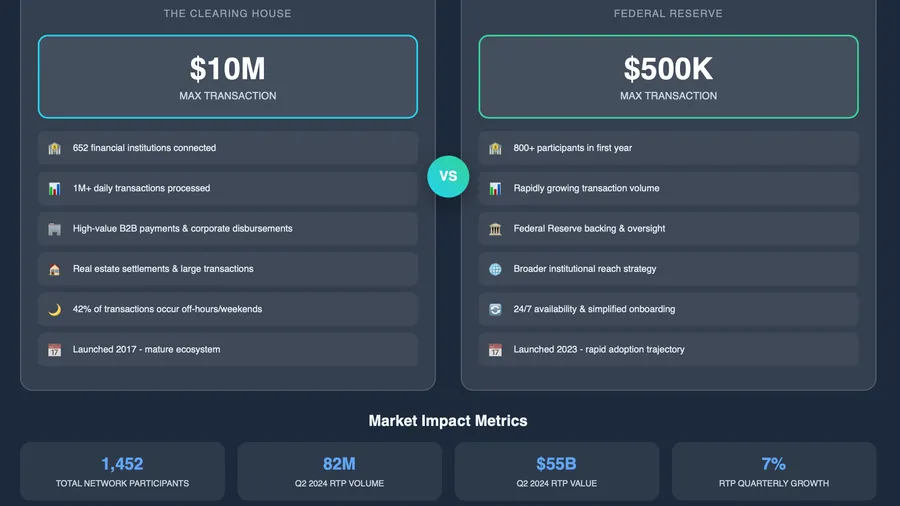

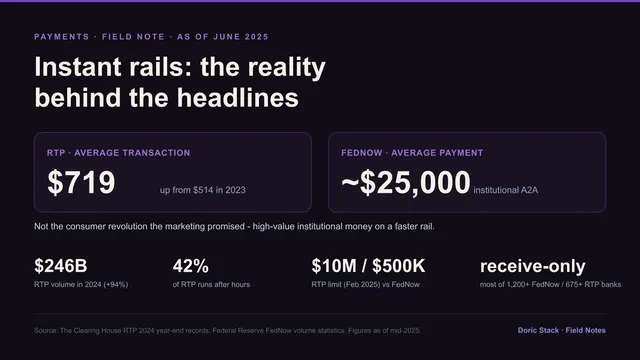

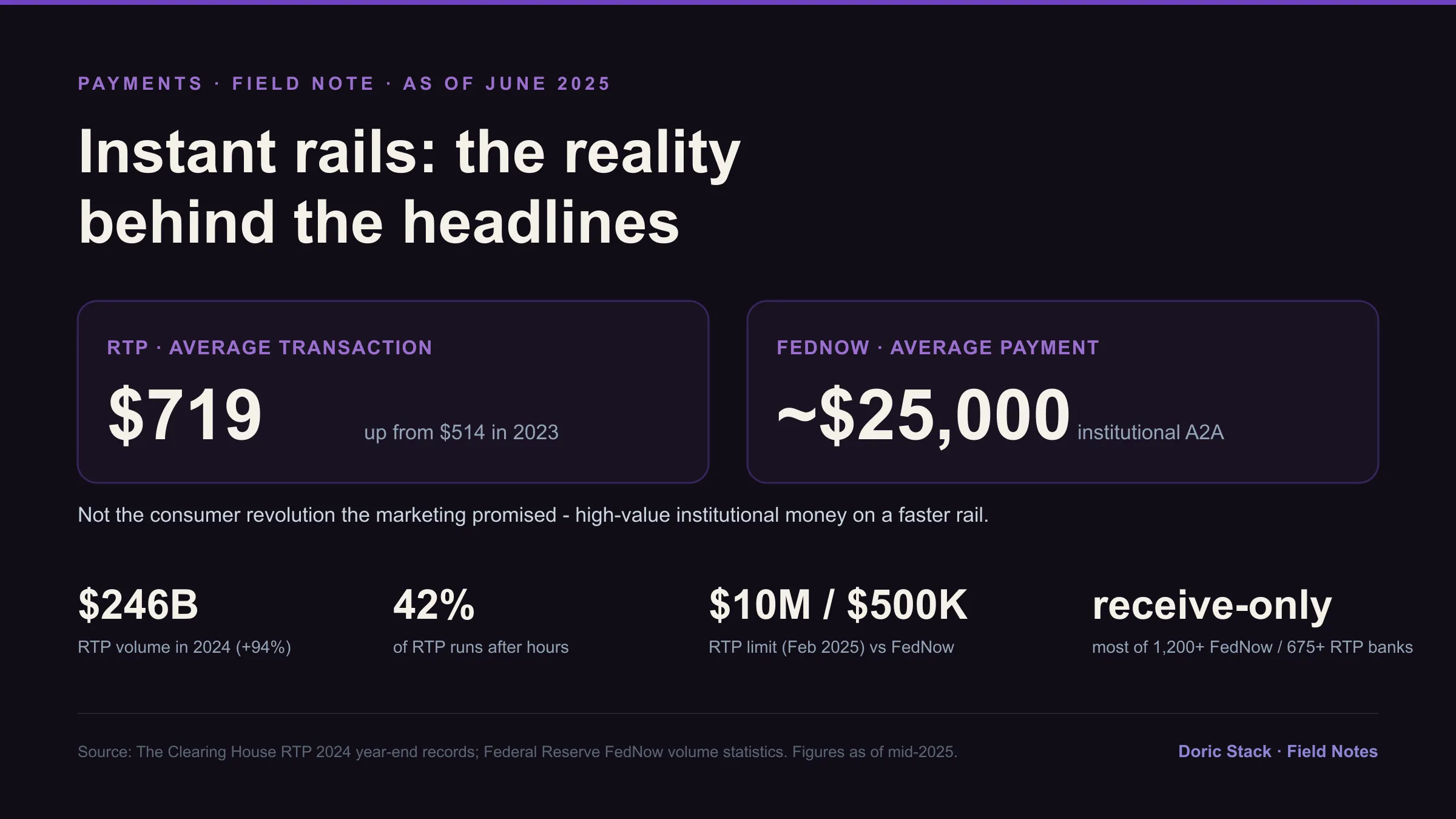

RTP processed $246 billion in 2024, up 94% year over year across 343 million transactions. FedNow reached $38.2 billion in its first full calendar year. “Instant payments are taking off,” the headlines said. The usage data tells a quieter, more useful story.

Marketing vs usage (June 2025)

The average-transaction gap, the volume and off-hours figures, the limit split, and the receive-only adoption pattern - the reality behind the adoption headlines.

Marketing vs usage (June 2025)

RTP average

$719

per transaction in 2024, up from $514 in 2023 - everyday-sized money (The Clearing House).

FedNow average

~$25,000

per payment in 2024 - corporate and brokerage account-to-account, not consumer (Federal Reserve).

Off-hours

42%

of RTP transactions land overnight, on weekends, or on holidays - the genuine 24/7 benefit.

The tell is in the averages. A $719 RTP payment is a bill, a payroll top-up, a gig payout. A ~$25,000 FedNow payment is a treasury sweep or a brokerage funding move. That is not consumers abandoning cards and ACH - it is high-value, low-volume institutional money finally getting a real-time option. Useful, but not the everyday-payments revolution the marketing implied.

What the marketing says

Instant payments are taking off. Record volume, near-100% growth, thousands of institutions signed up. The rails are here and adoption is exploding.

What usage shows

Most of the 1,200+ FedNow and 675+ RTP institutions are receive-only - they will accept an instant payment but will not send one. Banks are cherry-picking safe use cases and avoiding the operational complexity of full integration.

The infrastructure exists and the marketing sounds compelling. Actual usage says we are still years from instant being the default for everyday money.

This is selective implementation, not broad adoption. Banks are hedging - taking the receive side, leaning on 24/7 availability where it clearly pays (42% of RTP volume is already off-hours), and waiting on the rest. The recent split in transaction limits, RTP up to $10 million since February 2025 while FedNow’s default stayed at $500,000, only sharpens the sorting: the rails are increasingly chosen by transaction size, not by a wholesale move to real time.