As of June 2026

The payment is final in under a second. Your sanctions analyst is still opening the alert. On an instant rail there is no queue and no review window, so the screen has to clear or stop the payment in code, inside the rail's latency budget.

So build it like code: one screening policy, versioned and tested, with the action on a hit behind a strategy interface. The policy model can be common across rails. The lists, the match thresholds, and what a hit actually does are not, because a hit has to compile into whatever the rail allows.

Same verdict, different commit semantics

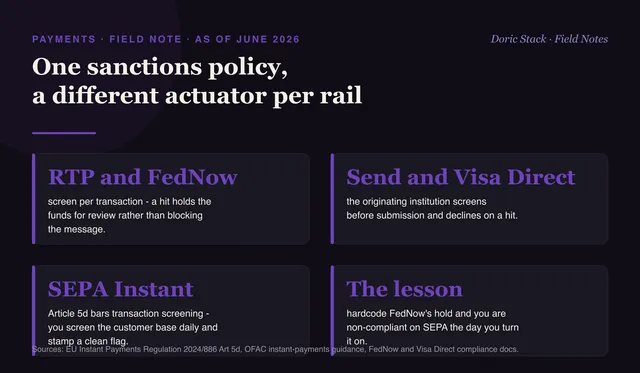

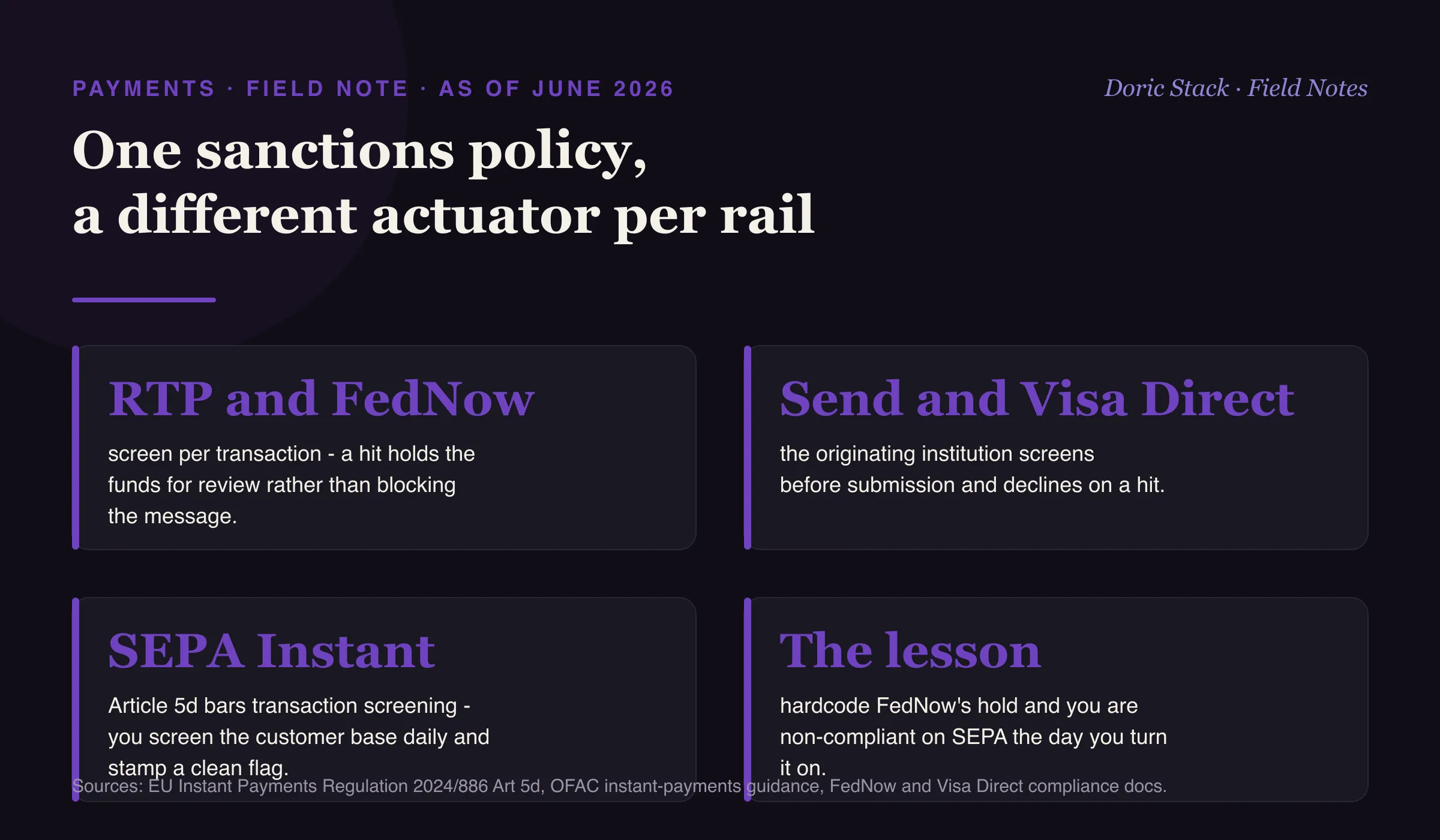

On TCH RTP and FedNow you screen per transaction, and a hit holds rather than blocks. The receiving institution accepts the message but not the funds and takes time to review, which on FedNow can stretch into the next business day as a matter of practice. Once the payment is final, clawing it back is a request the receiver can refuse. On Mastercard Send and Visa Direct the topology flips to the front: the originating institution screens the transfer before it is submitted to the network, and declines on a hit. Same sanctions verdict, a different point of control.

SEPA Instant inverts the whole thing

Article 5d of the EU Instant Payments Regulation makes screening the individual transaction during execution illegal. Instead you screen the customer base against the EU lists at least daily and immediately on every list update, stamp a clean flag, and the payment path becomes a single lookup. Same policy intent, a completely different topology.

RTP and FedNow

Hold

screen per transaction - a hit holds the funds for review rather than blocking the message at the network.

Send and Visa Direct

Decline

the originating institution screens the transfer before submission to the network and declines on a hit.

SEPA Instant

Article 5d

transaction screening is barred - you screen the customer base daily and the payment path becomes one lookup.

Sanctions screening as code is one policy that compiles to a different actuator per rail. Hardcode FedNow's hold and you are non-compliant on SEPA the day you turn it on.