As of December 2025

Instant rails now carry wire-sized money. In November 2025 FedNow raised its customer credit transfer limit from $1 million to $10 million, matching RTP, and layered in new risk controls. Instant is no longer coffee money.

Open the taps without new guardrails and every batch-era control gets a 24/7 bypass. The fraud checks, the liquidity monitoring, the dual approvals - all of it was built for a banking day that instant rails do not keep.

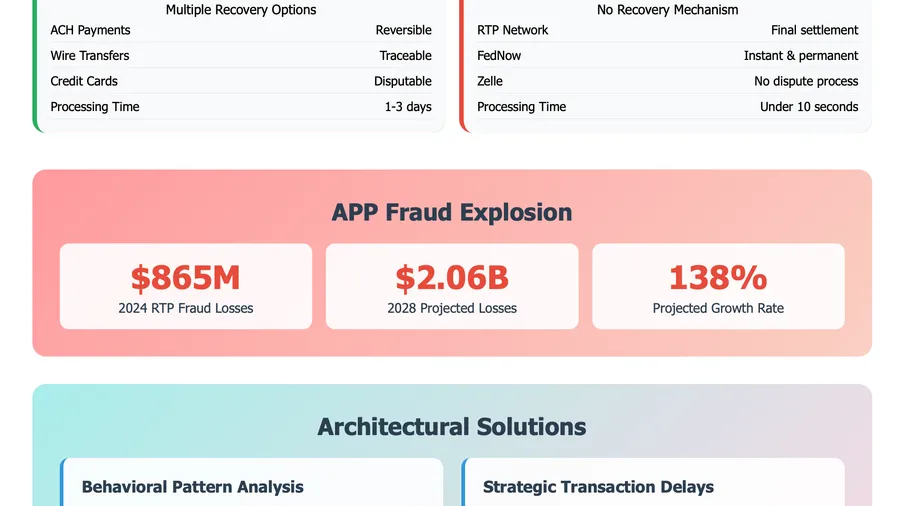

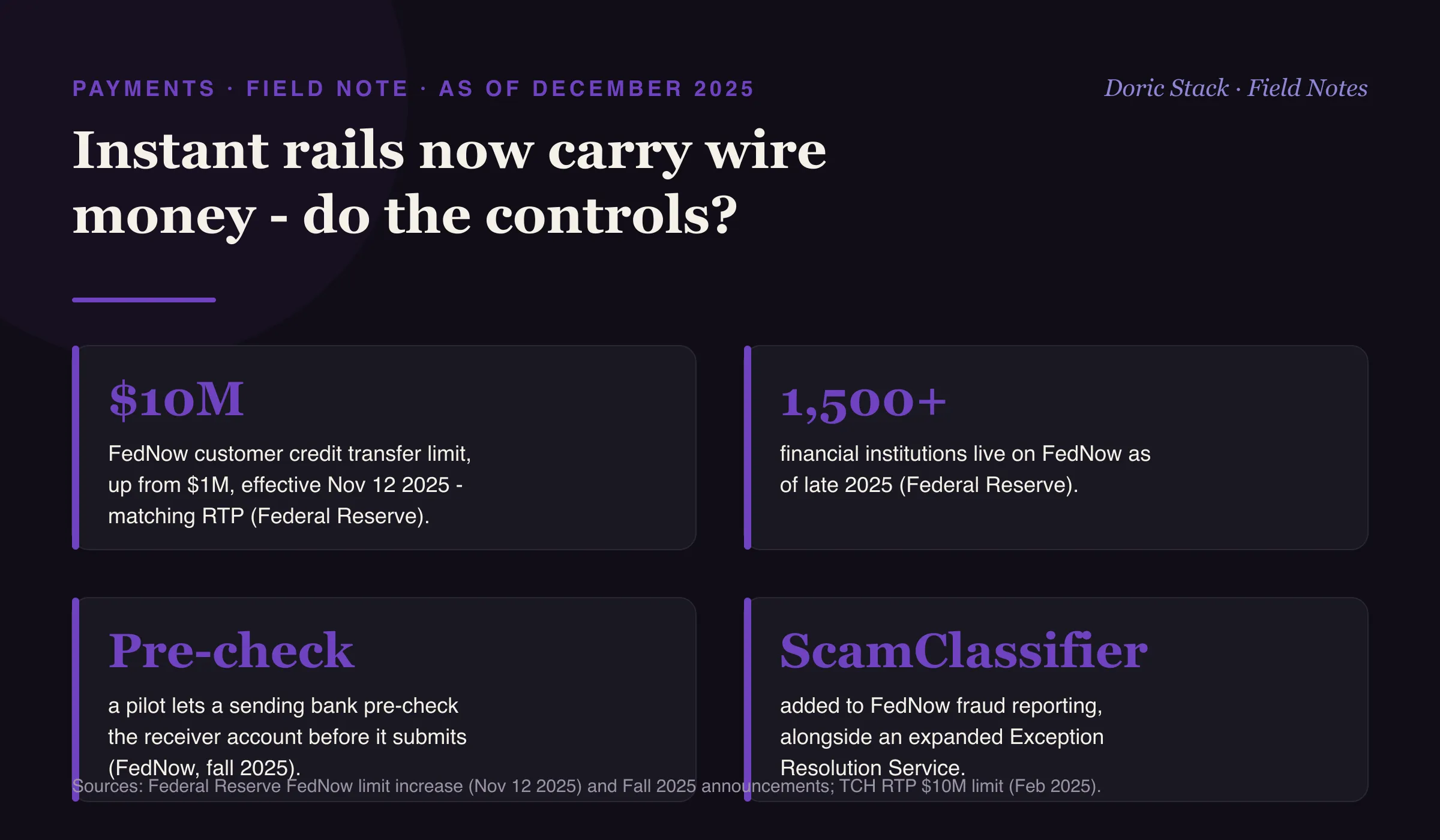

Alongside the limit increase, the Federal Reserve announced a cluster of fall 2025 controls: a pilot that lets a sending bank pre-check the receiver account before submitting, the ScamClassifier model added to fraud reporting, and the Exception Resolution Service expanded to FedNow transactions, with more than 1,500 institutions now live. The capability to run wire-grade money on instant rails is arriving. The controls have to arrive with it.

Network limit

$10M

FedNow customer credit transfer limit, up from $1M, effective Nov 12 2025, matching RTP (Federal Reserve).

Live participants

1,500+

financial institutions live on FedNow as of late 2025 (Federal Reserve).

New risk rails

Pre-check

a pilot lets a sending bank pre-check the receiver account before it submits (FedNow, fall 2025).

The batch-era assumption

Static dollar caps, overnight reconciliation, business-hour exception handling. Every one of them assumes the money waits for a banking day. At $10 million and 24/7, it does not.

The wire-grade stack to ship

Replace static caps with adaptive ceilings that move on value and velocity per customer and auto-drop to manual review on an anomaly spike. Use the pre-check as a gate, blocking when account status or name-number confidence fails and logging the payload to feed fraud analytics. Require a dual-confirm on a first high-value send to a new counterparty. Keep real-time liquidity buffers per rail with intraday sweeps between FedNow and core cash. Handle exceptions inside the rail, tagging suspected scams with ScamClassifier and coordinating reversals through the Exception Resolution Service. Then feed every exception and failed pre-check back into the rules within a day.