As of August 2025

For decades treasury ran on predictable timing: ACH overnight, wires in business hours, float you could model. Real-time rails removed the timing assumption entirely.

When a customer can move money instantly at any hour, the cash-positioning playbook built for batch processing stops working. FedNow and RTP did more than speed payments up. They took the schedule away.

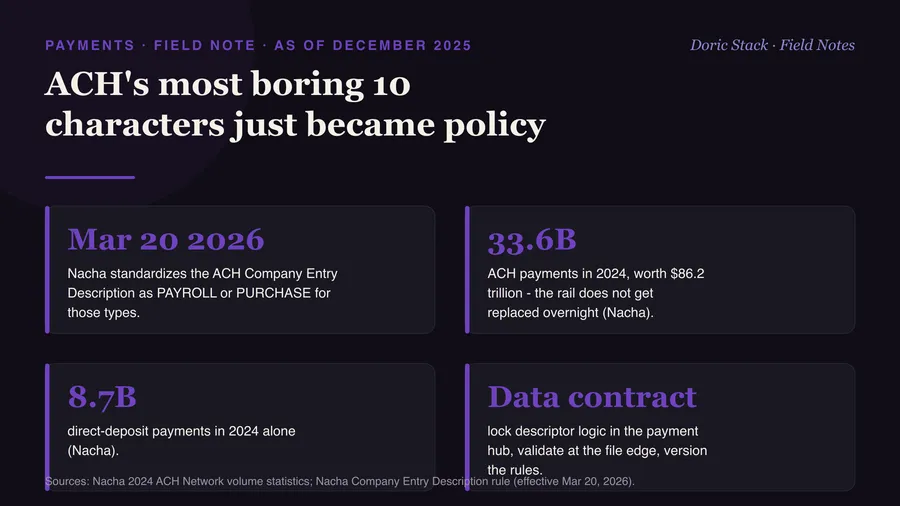

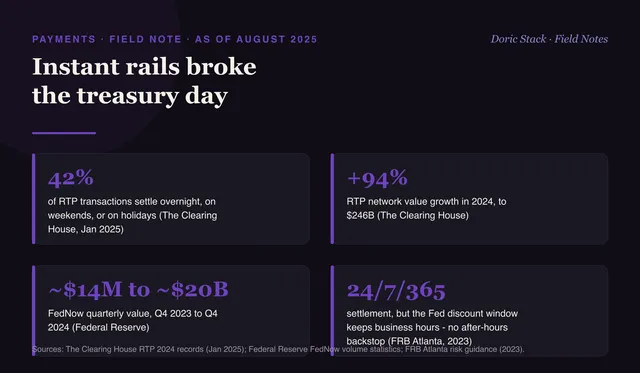

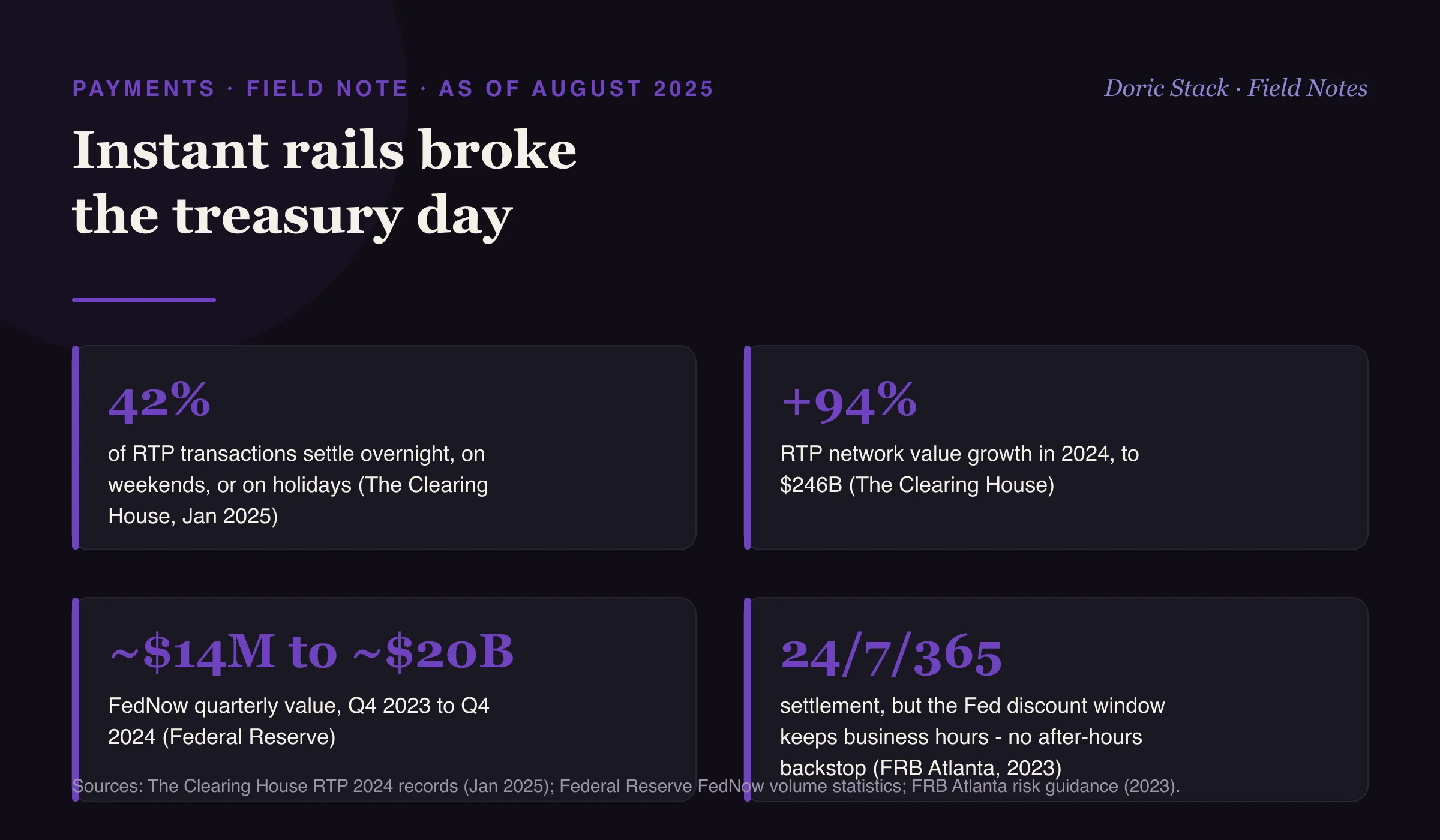

The numbers behind the shift are not gradual. RTP network value jumped 94 percent in 2024 to $246 billion, and FedNow went from roughly $14 million in quarterly value at the end of 2023 to about $20 billion a year later. The mix matters more than the totals: by The Clearing House’s count, 42 percent of RTP transactions now settle overnight, on weekends, or on holidays. A $2 million payment can land at 11 PM on a Friday and force an immediate liquidity decision with the markets closed and the usual funding sources shut.

Off-hours share

42%

of RTP transactions settle overnight, on weekends, or on holidays (The Clearing House, Jan 2025).

RTP value growth

+94%

RTP network value growth in 2024, to $246 billion (The Clearing House).

Fed backstop

Hours unchanged

the Fed discount window keeps business hours, so after-hours funding is not available (FRB Atlanta, 2023).

What stops working

Cash forecasting tuned for batch windows. Investment strategies that assume business-hour timing. Credit facilities scoped for 9-to-5. Risk frameworks built around deferred settlement. Every one of them quietly assumes money moves on a schedule, and that assumption is gone.

What replaces it

Hourly cash positioning instead of daily. Instant-payment reserves held separate from operating cash. 24/7 credit lines negotiated with correspondent banks ahead of need. Real-time analytics and alerting so a Friday-night inflow is a notification, not a Monday-morning surprise.

Real-time payments changed the operating model, not only the speed. The treasury teams still running batch-era assumptions are the ones that hit cash crunches at the worst possible moment.