As of December 2025

The most boring 10 characters in ACH just got promoted to policy. From March 20, 2026, Nacha requires the Company Entry Description to read PAYROLL or PURCHASE for those payment types.

It sounds trivial. A payroll file clears the window, then a small funding or account mismatch triggers returns and exceptions downstream, and one of the few consistent clues in the trail is that descriptor - too often a generic label like PAYRL_1025. Standardizing it changes how teams monitor, reconcile, and explain cash movement.

Effective

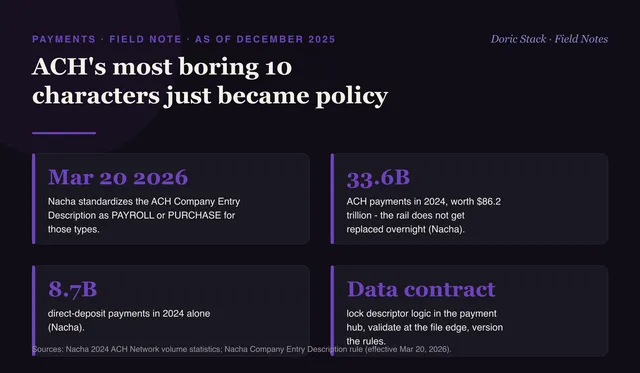

Mar 20 2026

Nacha standardizes the ACH Company Entry Description as PAYROLL or PURCHASE for those payment types.

ACH scale (2024)

33.6B

ACH payments worth $86.2 trillion - the rail does not get replaced overnight (Nacha).

Direct deposit

8.7B

direct-deposit payments in 2024 alone (Nacha).

Why a label is architecture

A reliable category survives the whole journey - from the ERP that originates the file, to bank operations, to the reconciliation engine that has to match it. When PAYROLL means payroll on every file, monitoring and exception workflows can key off it, and the automation that kept slipping on free text finally holds. A messy field becomes a dependable one, and that is the difference between rules that fire and rules that guess.

Why ACH still carries it

This matters because ACH is not going anywhere. In 2024 it moved 33.6 billion payments worth $86.2 trillion, with direct deposit alone at 8.7 billion. Batch fits treasury - predictable reconciliation windows, file-based payroll, known returns. Instant rails need always-on liquidity and staffing many teams do not have yet. The real picture is coexistence, with ACH the default for high-volume predictable flows.

Descriptors are now architecture, not metadata. When the label becomes reliable, the automation that kept slipping on free text finally holds.