As of June 2025

This is not a SWIFT killer story. It is an evolution toward a hybrid book, where high-value flows stay on SWIFT and newer rails take the jobs they are genuinely better at.

Payment headlines are full of the claim that XRP and RLUSD will replace SWIFT’s “outdated” network. As someone who designs payment architectures for banks, my read is the opposite: not replacement, evolution.

The pain points are real, and I see them daily. Cross-border wires taking 3 to 5 days when an instant rail settles in seconds. Multiple correspondent banks stacking cost and complexity. Manual processes turning into operational headaches. That frustration is exactly what fuels the “SWIFT is finished” story.

But the frustration and the conclusion are two different things. SWIFT is not going anywhere soon. That does not mean blockchain is irrelevant to payments. It means the interesting work is not picking a winner - it is deciding which rail does which job.

The signals on the right are why this is worth watching now, not later: a regulated stablecoin is growing fast enough to register as institutional adoption, and the incumbent has put a hard date on its own modernization.

The question is not whether blockchain will disrupt payments. It is whether we will lead that transformation or get dragged into it.

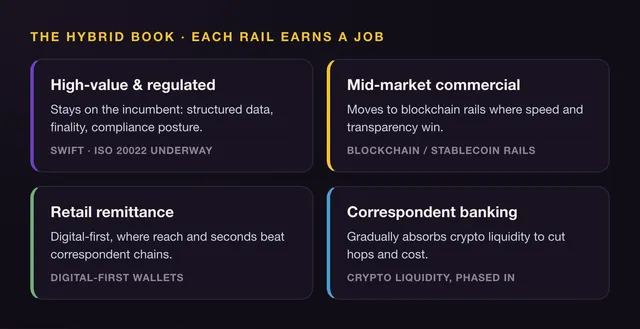

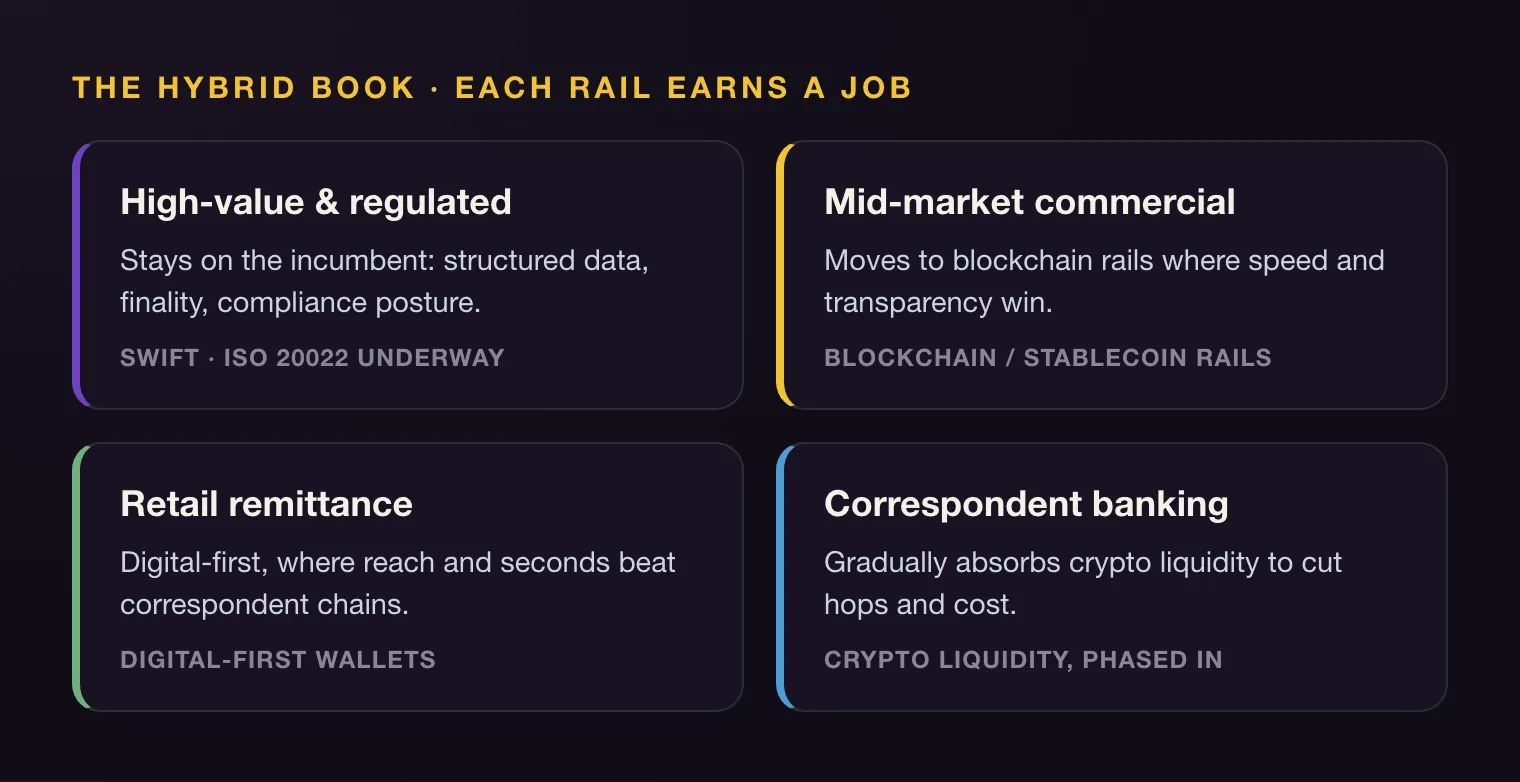

The hybrid book

Most banks will land on a hybrid approach rather than a single rail. The useful way to hold it in your head is not “old versus new” but four jobs, each going to the rail that does it best.

High-value regulated transactions stay on SWIFT, where structured data, finality, and compliance posture matter most. Mid-market commercial payments move to blockchain rails where speed and transparency win. Retail remittances go digital-first, where reach and seconds beat correspondent chains. And correspondent banking gradually absorbs crypto liquidity to cut hops and cost. None of that requires SWIFT to lose. It requires each rail to earn a specific job.

Why the incumbent is not the loser people expect

The “SWIFT killer” framing assumes the incumbent is frozen. It is not. SWIFT’s ISO 20022 migration is moving the cross-border network toward structured, richer payment data, and the MT/MX coexistence window is scheduled to close in November 2025. The gap that blockchain advocates point to - thin, unstructured messaging - is the exact gap SWIFT is closing without changing the rail underneath.

On the other side, the signal worth watching is not a price chart. RLUSD near a $244M market cap with roughly 87% month-over-month growth says institutions are beginning to treat regulated stablecoins as plumbing, not a speculative sideshow. Early, yes. But it is the kind of adoption curve that turns into a settlement leg, not a slogan.

The real opportunity was never the “SWIFT killer.” It is building payment rails that deliver the speed and transparency customers want while working alongside the infrastructure that already moves the world’s money. Lead that transformation, or get dragged into it.