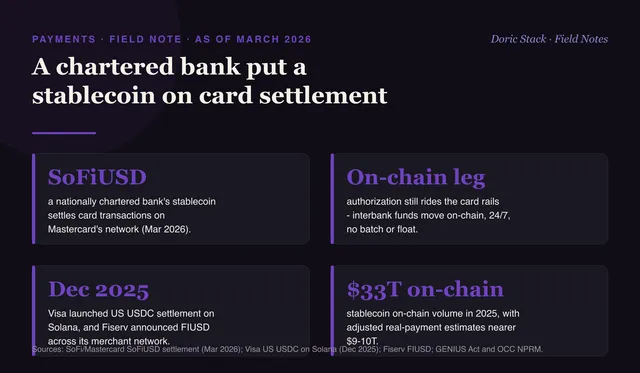

As of March 2026

A nationally chartered, FDIC-insured bank just put a stablecoin on Mastercard's settlement layer. SoFi Bank's SoFiUSD - an ERC-20 token on Ethereum, backed one to one by cash and short-term US Treasuries - now settles card transactions across the network.

That is not crypto news. It is settlement-architecture news. The reported first stablecoin from a nationally chartered bank on a public, permissionless blockchain, doing the least glamorous job in payments: moving money between banks.

What actually changed

Card settlement has worked the same way for decades. A merchant batches at end of day, the acquirer and issuer clear through the network, funds move T+1 or T+2 through correspondent accounts, and everyone reconciles the next morning. SoFiUSD swaps only the settlement leg. Authorization still rides Mastercard’s rails and the merchant experience does not change, but the interbank fund movement happens on-chain, around the clock, with no batch window and no correspondent float.

Why it matters beyond one bank

Issuers and acquirers get to choose their settlement medium for the first time. Stablecoin settlement collapses the credit-risk window between authorization and funding, acquirers see cash positions in real time instead of waiting for next-day files, and cross-border flows can avoid the 1-to-3 percent FX spread baked into correspondent chains. SoFi is not alone: Visa launched US USDC settlement on Solana in December 2025, and Fiserv announced FIUSD across its network of six million merchant locations.

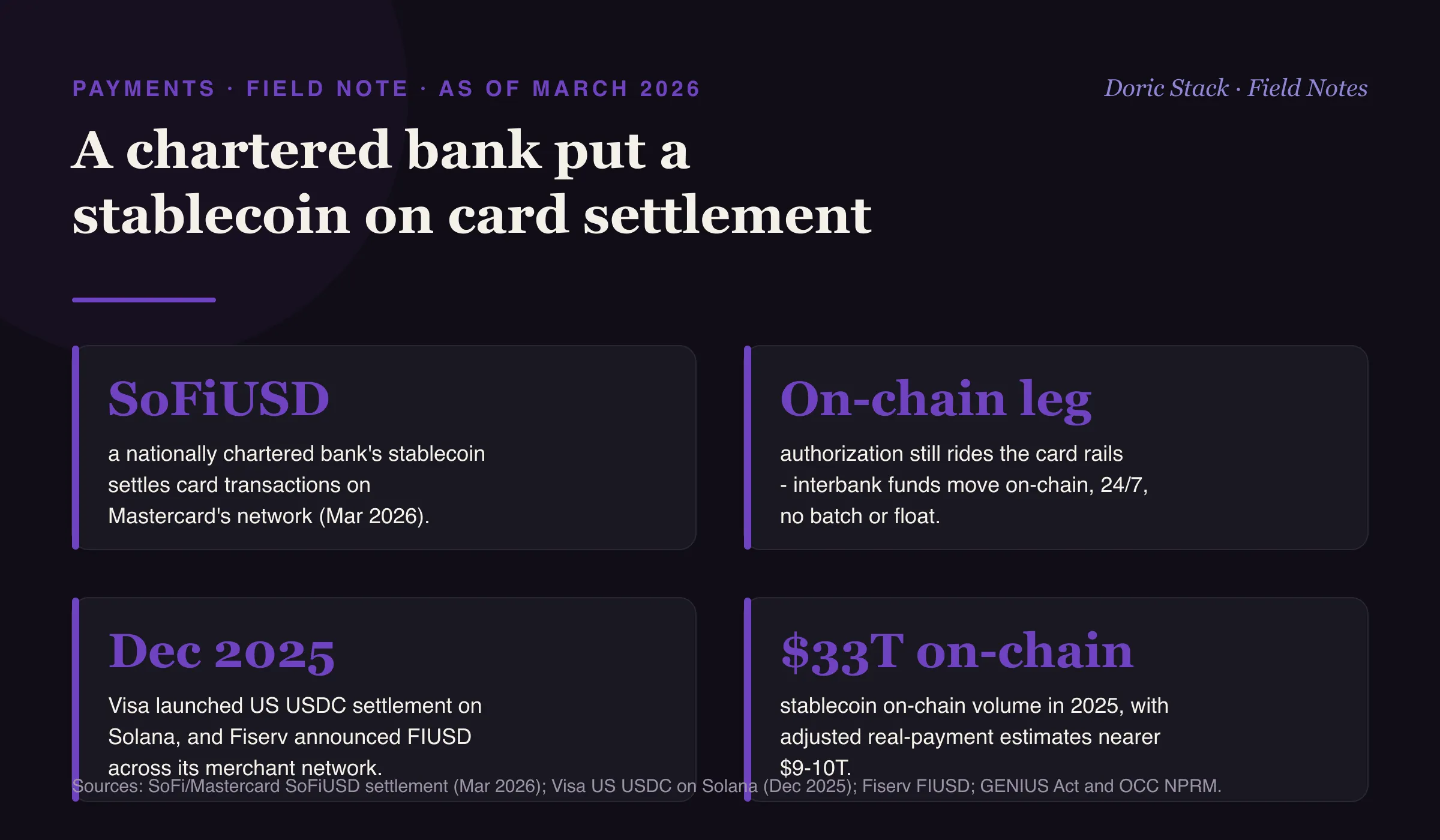

What launched

SoFiUSD

a nationally chartered bank's stablecoin settling card transactions on Mastercard's network (Mar 2026).

The swap

On-chain leg

authorization still rides the card rails, but interbank funds move on-chain, 24/7, with no batch or float.

2025 volume

$33T on-chain

stablecoin on-chain transfer volume in 2025, with adjusted real-payment estimates nearer $9 to $10T.

The blockchain is not the story. The story is that issuers and acquirers can choose their settlement medium for the first time, and the infrastructure is opt-in - nobody changes anything unless the economics make sense.