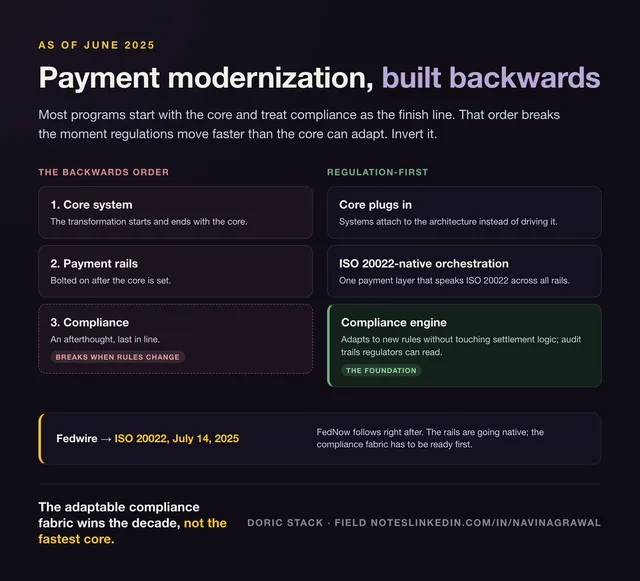

As of June 2025

Start with compliance as your foundation, not your finish line. With Fedwire going ISO 20022-native this summer, a core-first modernization is building the house from the roof down.

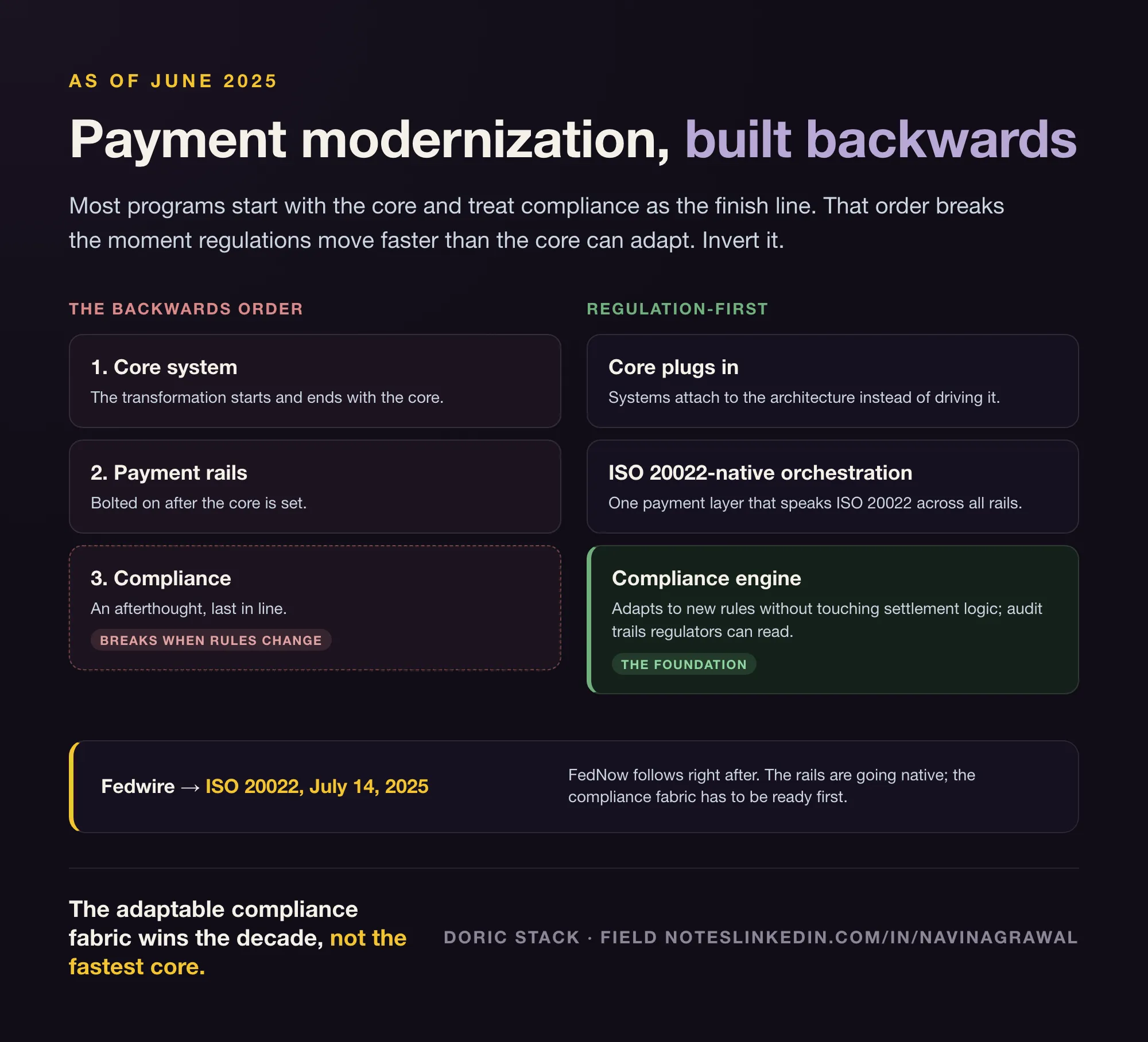

I keep seeing banks run modernization programs in the same backwards order: core system first, payment rails second, compliance last. It looks orderly. It breaks the first time a regulation moves faster than the core can adapt.

There is a clock on this. Fedwire flips to ISO 20022 on July 14, 2025, and FedNow follows right after. The messaging layer of the US high-value and instant rails is going structured and native, and every bank touching those rails inherits that change regardless of where its core modernization happens to be.

That is exactly why the usual sequence is wrong. If compliance is the last thing you bolt on, then every new requirement - a fresh AML rule, a sanctions change, a reporting mandate - lands on an architecture that was never designed to absorb it. I have watched beautiful technical architectures crumble when new AML requirements dropped. The ones that survived had a flexible compliance layer underneath, not a fast core on top.

The banks with the most adaptable compliance fabric will dominate the next decade - not the ones with the fastest cores.

The regulation-first blueprint

Invert the stack. Put the parts that change most often, and cost the most when they break, at the bottom.

The inverted stack (June 2025)

The backwards order versus the regulation-first order, and the July 2025 Fedwire ISO 20022 trigger that makes the sequencing urgent.

The inverted stack (June 2025)

Why the order is the whole argument

The blueprint that actually holds up has four moves. A compliance engine that adapts to new rules without touching settlement logic. A payment orchestration layer that speaks ISO 20022 natively across all rails, so a rail going native is a configuration event, not a re-platform. Core systems that plug into that architecture instead of driving it. And audit trails your regulators can actually read, designed in from the start rather than reconstructed under pressure.

None of those four components is exotic. The argument is entirely about sequence. Core-first means the compliance and orchestration layers have to bend around decisions the core already locked in. Compliance-first means the core is a replaceable participant in an architecture that already knows how to absorb a rule change or a rail migration.

The trigger

Fedwire goes ISO native

Fedwire moves to ISO 20022 on July 14, 2025, with FedNow following. The rails are going native whether or not the rest of the stack is ready.

The common order

Core first

Most programs sequence core system first, payment rails second, compliance as an afterthought - and that order breaks when rules move faster than the core can adapt.

The call

Compliance is the floor

Start with an adaptable compliance fabric as the foundation. The banks with the most flexible compliance layer outlast the ones with the fastest core.

The controversial part is not the components. It is that the fastest core is the wrong thing to optimize for. The decade belongs to whoever can absorb the next regulation without a re-platform.