As of August 2025

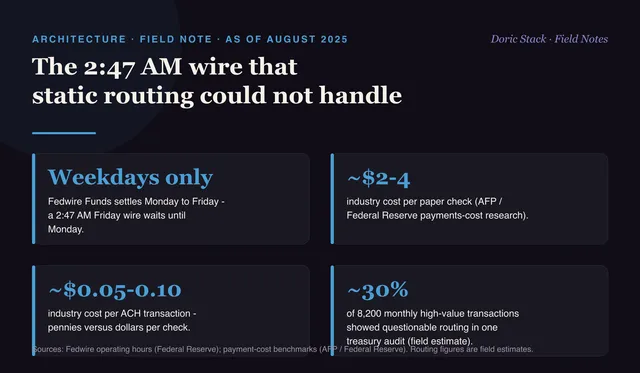

Static routing rules cannot read context. A high-value wire arrives at 2:47 AM Friday, the rule defaults to Fedwire because the amount is large, and Fedwire settles Monday to Friday - so the payment sits until Monday while contract penalties accrue.

The amount triggered the wrong rail. Nothing in the logic asked whether the timing worked, whether the destination bank could receive it, or what the delay would cost.

Three generations of payment thinking

Paper moved value with checks and armored trucks - slow, predictable, and dollars per item. Electronic rails dropped the cost to pennies but kept human-written routing rules. The next step is context-aware routing: instead of “large wire goes to Fedwire,” the logic weighs the customer’s SLA, the destination bank, the timing, and the penalty exposure, then picks the path.

Where static rules break

They optimize on one variable, usually amount, and ignore the rest. A rule that cannot tell 2:47 AM Friday from 2:47 PM Tuesday will keep routing weekend wires to a weekday-only rail. The rail is fine. The logic that cannot see the calendar is the problem.

The cost arc is what makes the case. Industry benchmarks put paper checks at a few dollars per item and ACH at pennies, a real collapse in unit cost, yet the decision layer on top barely changed. We moved the rails into software and left the routing logic in the 1990s.

Fedwire hours

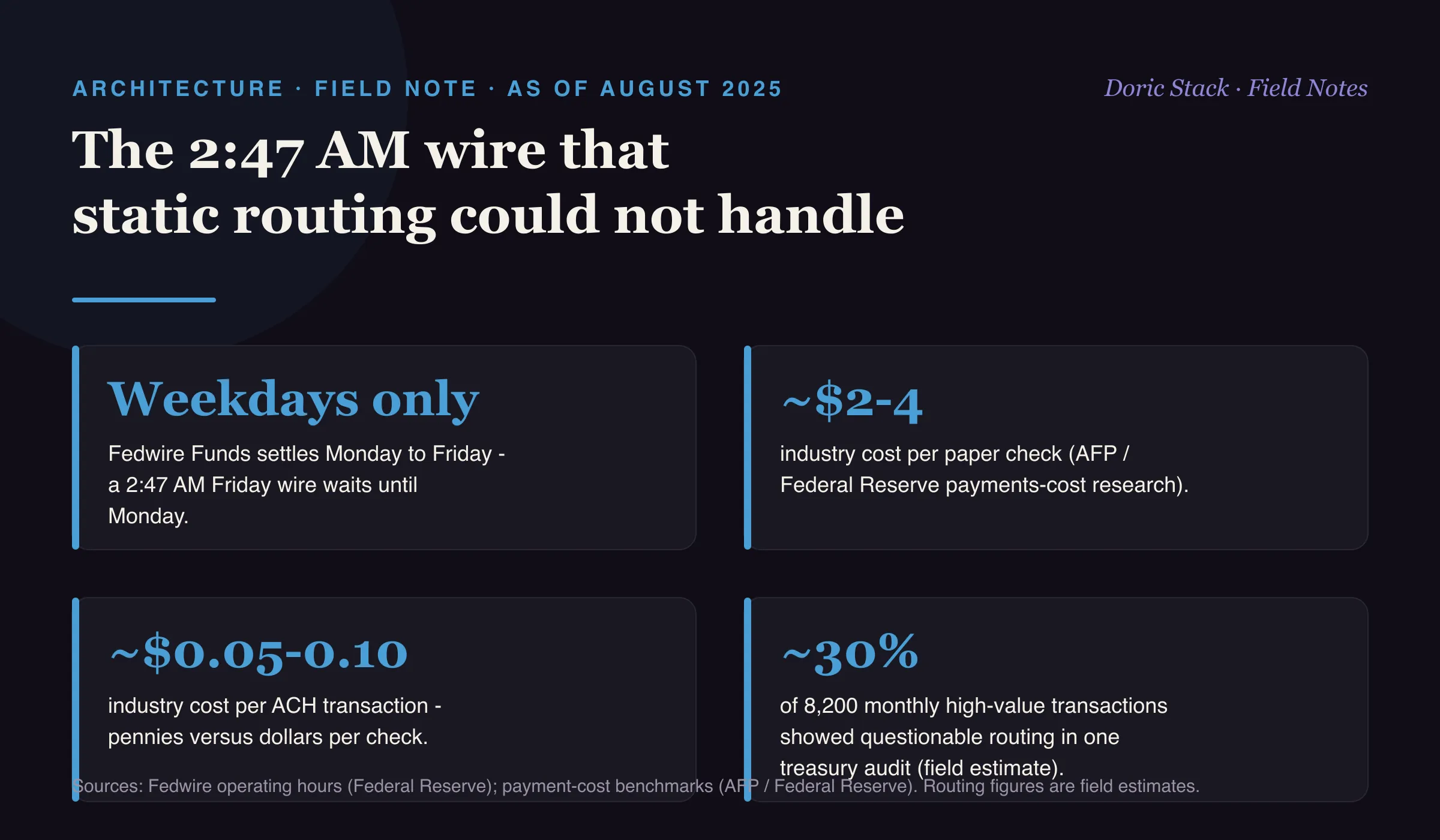

Weekdays only

Fedwire Funds settles Monday to Friday, so a 2:47 AM Friday wire waits until Monday.

Paper check

~$2-4

industry cost per paper check (AFP / Federal Reserve payments-cost research).

ACH

~$0.05-0.10

industry cost per ACH transaction - pennies versus dollars per check.

Manual routing decisions cannot compete with logic that reads the customer's SLA, the destination bank, and the calendar before it picks a rail.