As of May 2026

I keep coming back to one thought experiment on the BRICS payments debate. If local-currency corridors become mainstream, how would cross-border payment architecture actually change? Not geopolitics, and not SWIFT is dead. The practical question is simpler.

When a US company pays a supplier in a BRICS country, does the payment still default to USD correspondent banking, or does the payment hub choose the corridor before release? That single decision, made before money moves, is where the architecture changes.

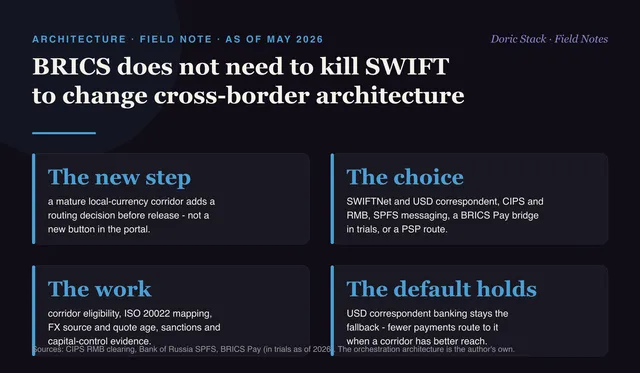

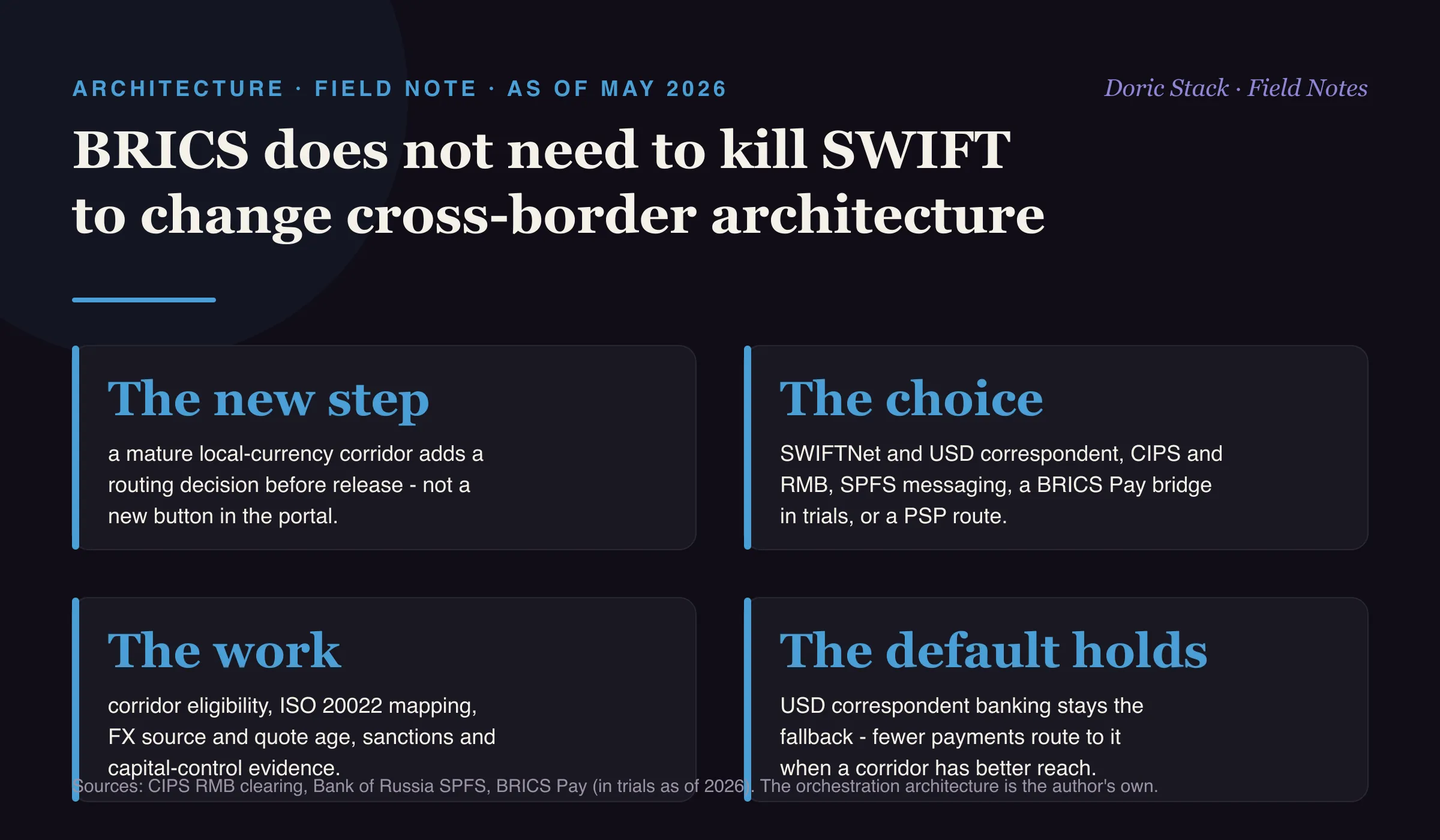

Today that supplier payment usually starts in ERP or treasury. The payment hub validates the instruction, treasury funds USD or books FX, SWIFTNet carries the bank message, and correspondent accounts and local clearing get the money to the supplier. That path does not vanish. What a mature local-currency corridor adds is a decision before release: should this payment use SWIFTNet and USD correspondent banking, CIPS and RMB settlement, SPFS messaging, a BRICS Pay bridge in the corridors where trials have started, or a PSP route? That is not a new button in the portal. It is middleware, policy, liquidity, and evidence.

What the corridor decision needs

The decision layer is not glamorous. It needs corridor eligibility rules, ISO 20022 mapping across networks that do not share a dialect, an FX source with a quote age you can defend, local-currency liquidity actually positioned where the payment lands, sanctions and capital-control evidence captured at decision time, message acknowledgment and status tracking, and one case ID that survives from initiation to settlement.

Where the systems actually stand

CIPS is live for RMB cross-border clearing and SPFS is Russia’s financial-messaging alternative to SWIFT, both real and in use. BRICS Pay, with its DCMS messaging layer, is still in trials rather than a production rail, so it is a design target, not a default. Blockchain may appear in CBDC or tokenized settlement corridors, but it is not the answer to most of this. The near-term work is payment orchestration, message translation, evidence, and reconciliation.

The new step

Route then release

a mature local-currency corridor adds a routing decision before release, not a new button in the portal.

The default

USD holds

USD correspondent banking stays the fallback - fewer payments route to it when a corridor has better reach.

The hard part

Evidence

explaining why this currency, this message network, this FX source, and this path before money left the bank.

BRICS does not need to kill SWIFT to matter. The shift is fewer payments defaulting to USD routing when a local-currency corridor has better liquidity, legal coverage, and settlement reach.