As of June 2026

Five central banks are quietly testing a settlement platform that does not touch SWIFT or the dollar. The headlines treat that as the end of dollar dominance. The numbers treat it as a pilot. Both are looking at the same thing.

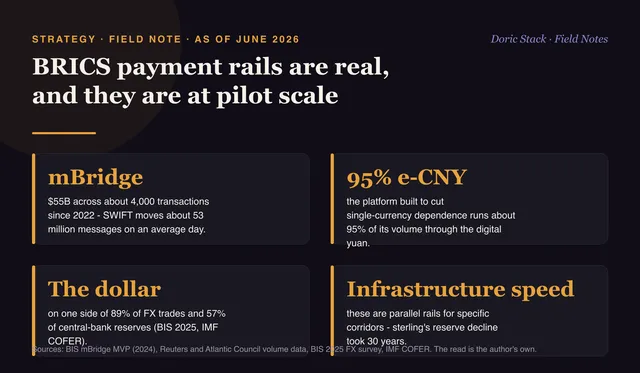

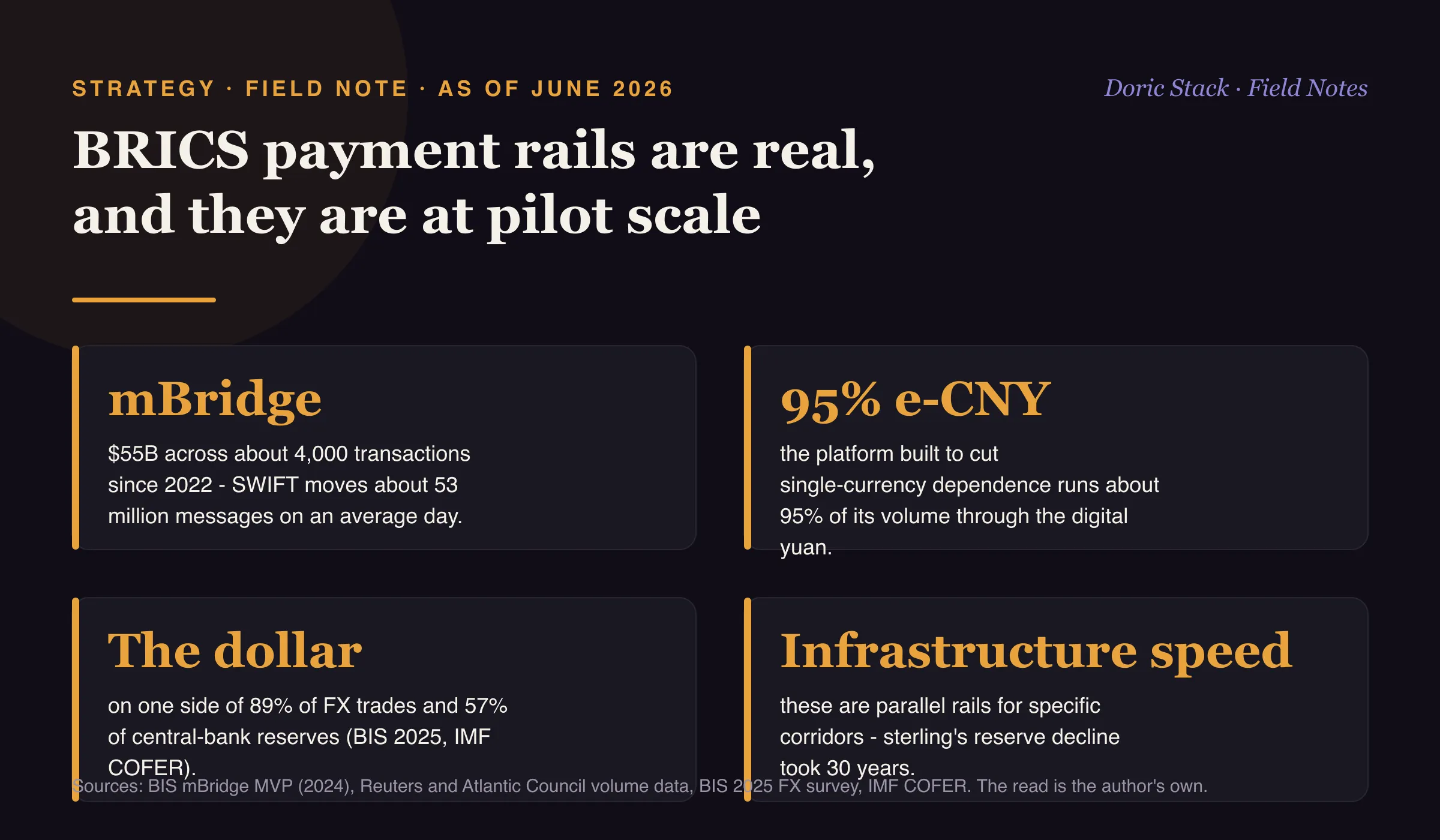

mBridge has been live since its 2022 pilot, with the People’s Bank of China, the Hong Kong Monetary Authority, the Bank of Thailand, and the Central Bank of the UAE, joined by Saudi Arabia at the minimum-viable-product stage in mid-2024. Total volume to date is around 55 billion dollars across roughly 4,000 transactions. For scale, SWIFT moved about 53 million messages on an average day in 2024.

What the platform actually is

mBridge is a multi-central-bank digital currency settlement platform, real and running, not vaporware. It reached minimum viable product in mid-2024. The Bank for International Settlements helped build it for about four years and then exited in October 2024. Its general manager, Agustin Carstens, said the reason was project maturity, that the partners could carry it forward on their own, and he publicly rejected the idea that mBridge was a BRICS or sanctions-evasion vehicle, noting only that the BIS does not operate with sanctioned jurisdictions. Read against the timing, the exit still tells you the project sits on politically sensitive ground, which is my own read rather than the BIS position.

The irony is in the composition. The platform built to reduce dependence on a single dominant currency runs about 95 percent of its volume through China’s digital yuan, per Atlantic Council analysis. One concentration risk has been swapped for another.

The roadmap is long

India holds the 2026 BRICS chairmanship and has put cross-border CBDC linkage on the summit agenda. A research institute, not a central bank, launched a gold-backed pilot settlement unit, roughly 40 percent gold, in October 2025. Russian officials keep pushing for a working system, and the timelines analysts attach to it run toward 2030. In government infrastructure years, that probably means later still.

mBridge to date

$55B

about 55 billion dollars across roughly 4,000 transactions since 2022, per Reuters and Atlantic Council data.

SWIFT, an average day

53M msgs

SWIFT moved about 53 million messages a day in 2024 - mBridge is a rounding error against that baseline.

The dollar

89% / 57%

on one side of 89 percent of FX trades (BIS 2025) and 57 percent of allocated reserves (IMF COFER).

These are parallel rails at pilot scale. They matter for specific corridors and route around the existing system in targeted spots. They do not replace it. Infrastructure moves at infrastructure speed, not headline speed.