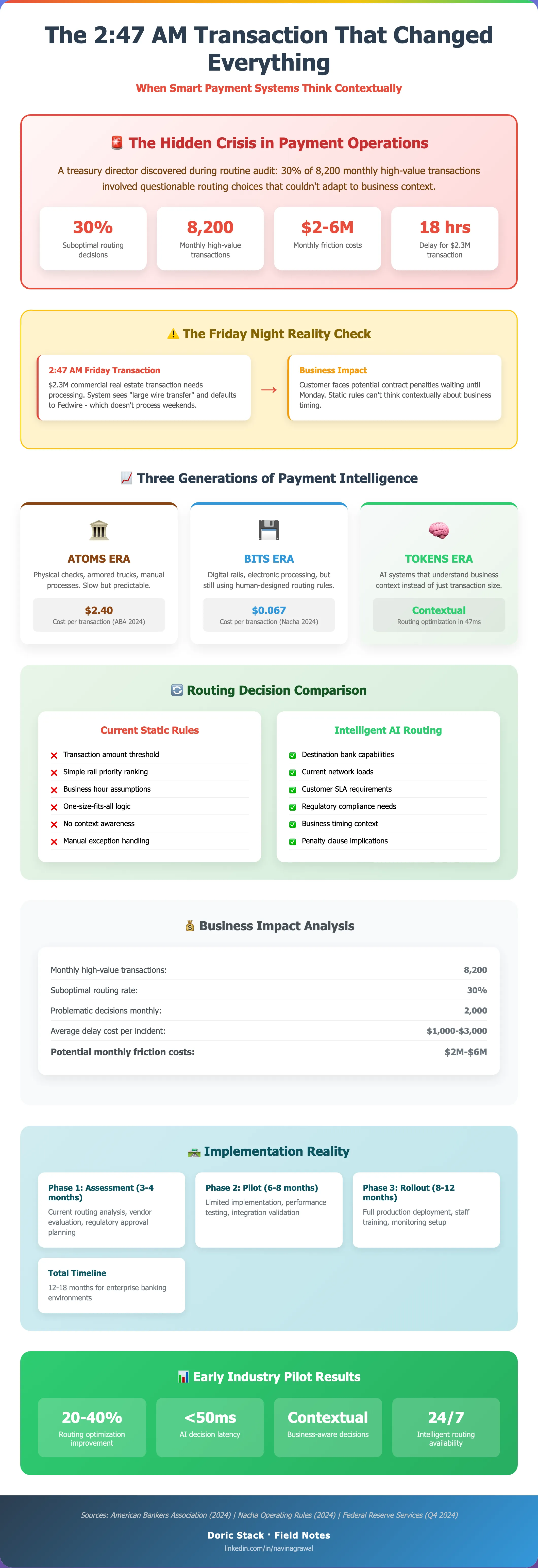

Thesis

The useful AI layer in banking is not the interface. It is the decision fabric beneath the payment.

Customer-service bots are visible. Routing intelligence is valuable. It sits at the moment where a payment objective becomes a rail decision, and it can explain why one path is safer, faster, cheaper, or more appropriate than another.

Rail choice

Fedwire, RTP, FedNow

Each rail exposes a different model for settlement, availability, reach, limits, and exception handling.

Decision moment

Before execution

The routing layer matters when it scores the payment path before the payment leaves the bank.

Operating model

Policy plus telemetry

A credible system combines product policy, live rail signals, liquidity posture, and audit evidence.

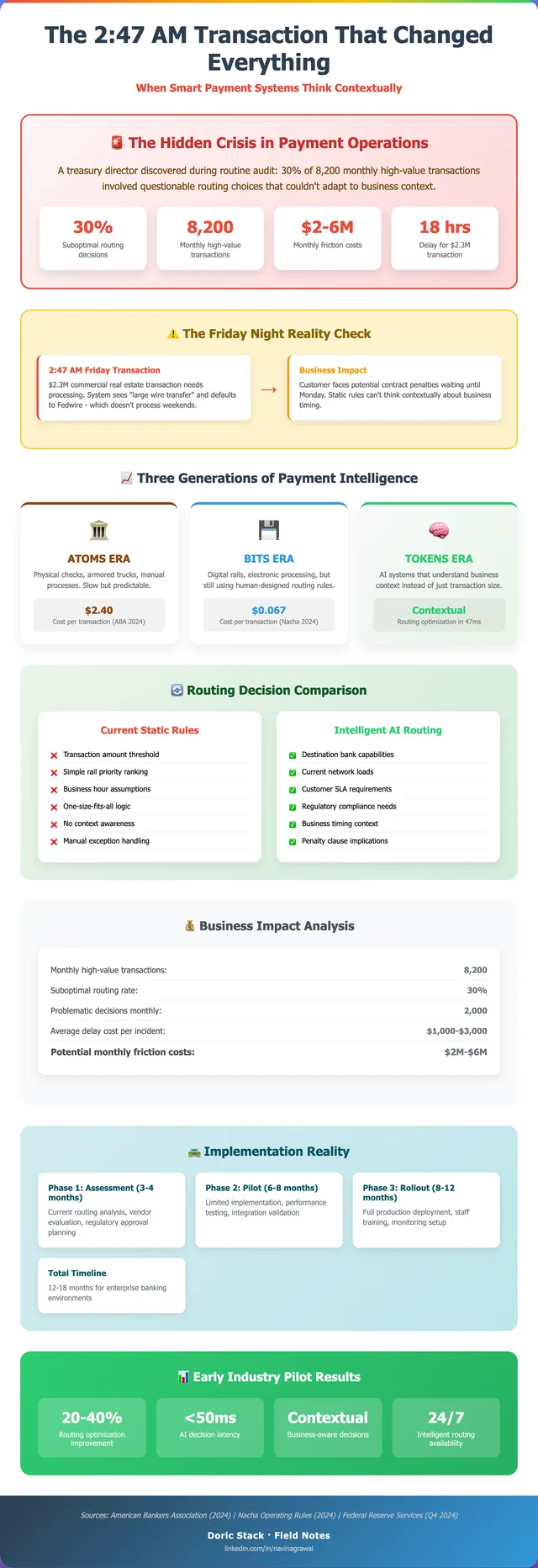

Everyone talks about GenAI in banking through the front door: chatbots, document summarization, agent assist, onboarding help. Those are real use cases, but they are not where the hardest payment architecture work sits.

The harder problem is buried inside payment operations. When money needs to move, a bank or platform must choose a path. That choice is not one-dimensional. Speed matters. Cost matters. Reach matters. Finality matters. Risk controls matter. Liquidity matters. So does the operating window of the rail and the receiver’s ability to accept the payment.

That is why payment routing is a better AI story than another natural-language interface. It is a live decision problem with policy, constraints, telemetry, and accountability.

Routing decision map

The decision layer is useful only when it shows the path from payment intent to rail choice, with evidence left behind for operations and audit.

Intent

01

Capture the payment objective

Amount, urgency, counterparty, refundability, operating window, and failure tolerance define the route search.

Eligibility

02

Filter by reachable rails

Instant payments, real-time gross settlement, and legacy rails do not expose the same participation, limit, or operating model.

Scoring

03

Score the viable paths

The model compares settlement speed, cost, liquidity effect, operational risk, and exception handling before execution.

Execution

04

Route with evidence

The chosen path should leave an audit trail: why this rail, why now, and what fallback was available.

The routing decision

Take a commercial payment that could fit more than one rail. One path may offer real-time clearing. Another may provide a different settlement and operational model. A third may be more familiar to the existing treasury process. Static routing tables often flatten that decision into a default.

That default can be wrong for the moment.

An intelligent routing fabric asks better questions before execution: can the receiving institution accept this rail, is the amount eligible, what is the settlement expectation, what exception path exists, what is the liquidity effect, and what policy applies to this customer or payment type?

Why this is an AI problem

Rules still matter. In payments, they matter more than hype does. A bank cannot hand a routing decision to a model that ignores limits, finality, sanctions screening, customer entitlements, or operational risk.

The AI layer earns its place when it works inside those constraints. It can rank paths, detect changing conditions, learn from exception history, and surface why a recommended route fits the payment objective. The output should be a decision with evidence, not a mysterious answer.

That distinction matters. A routing model that cannot explain itself is a compliance problem waiting to happen. A routing model that cites the constraints it used becomes an operations asset.

Decision artifact

The hero preview shows the problem. This full artifact shows the operating model: intent, eligibility, scoring, execution, and audit feedback.

Decision artifact

Where the value shows up

The first win is not a magical settlement claim. It is removing bad defaults. If two rails are viable and one better matches urgency, availability, cost, or risk posture, the system should make that choice with a trace.

The second win is operational. Exceptions teach the routing layer. Failed availability checks, returned payments, receiver limitations, cutoffs, support tickets, and liquidity frictions become feedback. Over time, the route decision becomes less generic and more institution-aware.

The third win is product design. A platform that understands payment intent can present better options to the user before execution: pay now, pay later, use this rail, split the payment, require approval, or hold until a safer window. That is a premium banking experience because it changes the decision, not the copy around the decision.

The architecture advantage

The banks and platforms that get ahead will not be the ones with the flashiest assistant. They will be the ones that encode rail behavior, customer policy, treasury posture, and exception telemetry into a routing layer that can be tested.

That layer is hard to copy because it is not only a model. It is product policy, data quality, operational history, observability, and institutional muscle.

AI belongs here because the decision space keeps expanding. Fedwire, RTP, FedNow, ACH, card rails, internal ledger movement, wallet balances, and cross-border partners all carry different constraints. A human can set policy. A rules engine can enforce hard gates. A decision layer can score the viable paths in the moment.

That is the hidden AI opportunity in banking: not replacing payment operations, but giving them a better decision fabric.