As of July 2025

When the OpenAI CEO tells a room of bankers that AI has already beaten most of how people authenticate, the takeaway is not to harden voice systems. It is that an entire category of authentication is finished.

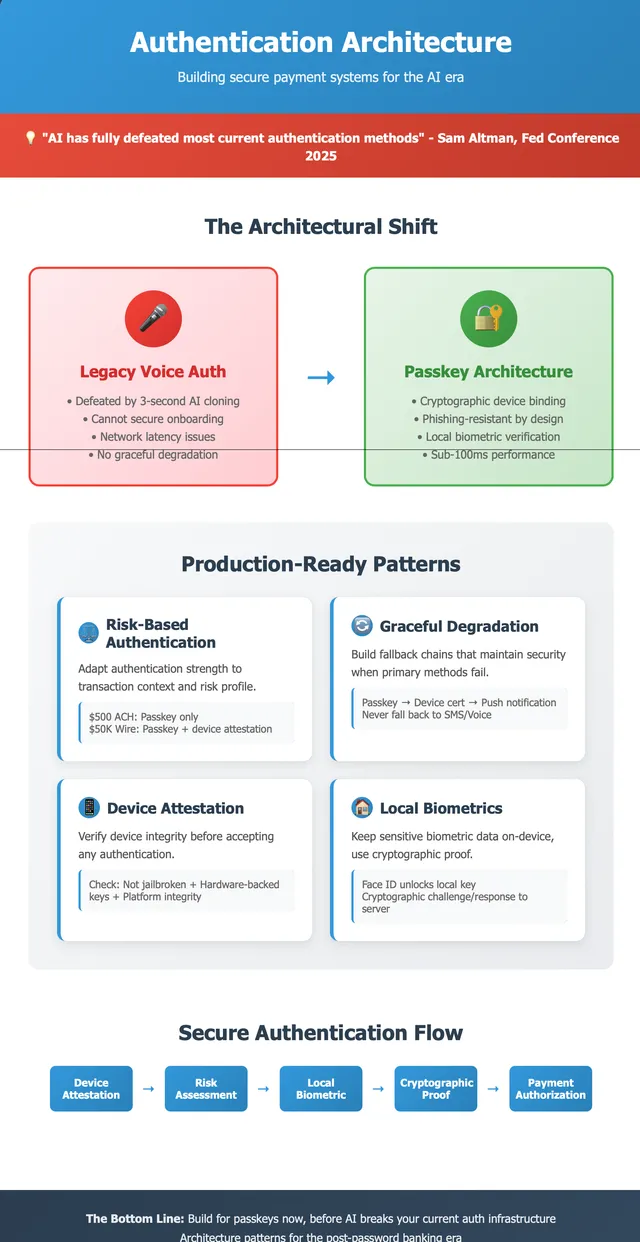

At a Federal Reserve conference on 22 July 2025, Sam Altman warned that “AI has fully defeated most of the ways that people authenticate currently other than passwords” - aimed squarely at the voiceprint systems some banks still accept. Modern voice cloning needs only a few seconds of audio to pass them.

The detail that should worry every bank: this was not a researcher’s hypothetical. Voice authentication that banks spent millions deploying is being bypassed by tools that clone a voice from a roughly three-second clip. When the Fed’s own Vice Chair for Supervision, Michelle Bowman, responded by floating partnerships with AI firms to help identify impersonations and deepfakes, it confirmed that the incumbent authentication stack is treated as broken, not patchable.

The replacement architecture is not exotic - passkeys use device-bound cryptographic keys instead of a shared secret or a sound the attacker can synthesize. But swapping authentication methods on a payment platform is an infrastructure problem as much as a security one, because real-time authorization still needs sub-100ms responses. The design has to be fast and resilient at the same time.

What is being retired

Voiceprints and any “something you sound like” factor. They are now an open door: a few seconds of recorded audio is enough to clone the credential, and no amount of “enhanced” voice modeling closes a gap that is fundamental to the method.

What replaces it

Risk-based, layered auth. A routine $500 ACH gets a passkey check; a $50K wire to a new beneficiary gets stepped up. Graceful degradation falls back to device-bound certificates and cryptographic push - never to SMS or voice. Biometrics stay local: the device unlocks the passkey, and no biometric data crosses the network.

The fix is not a better voice system. It is rebuilding authentication around keys that cannot be cloned from a recording - and doing it before the next breach forces the issue.